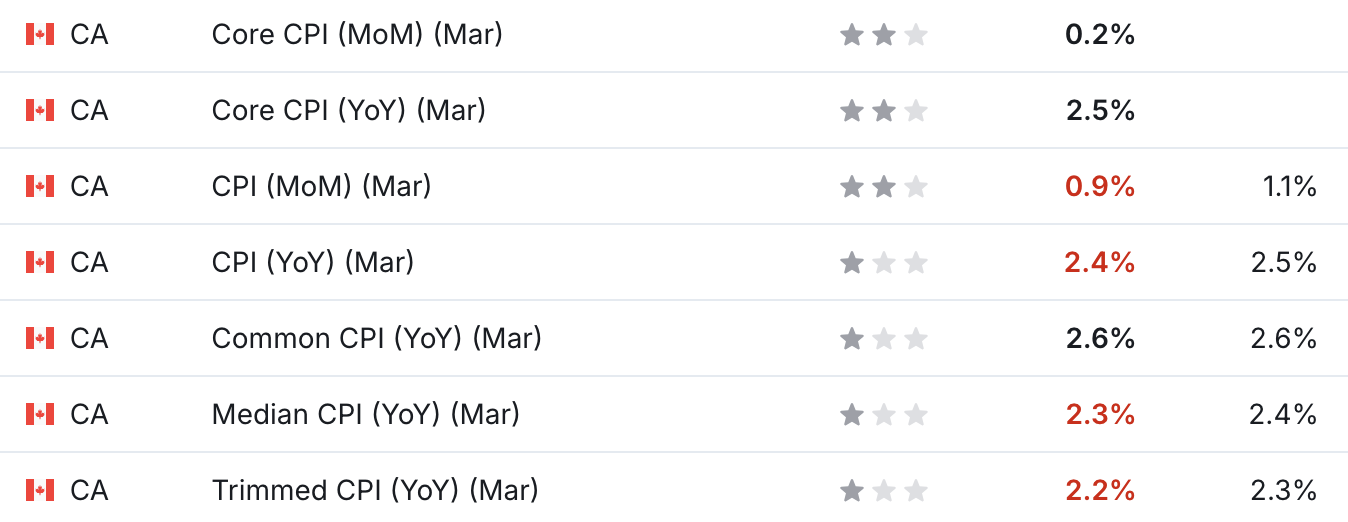

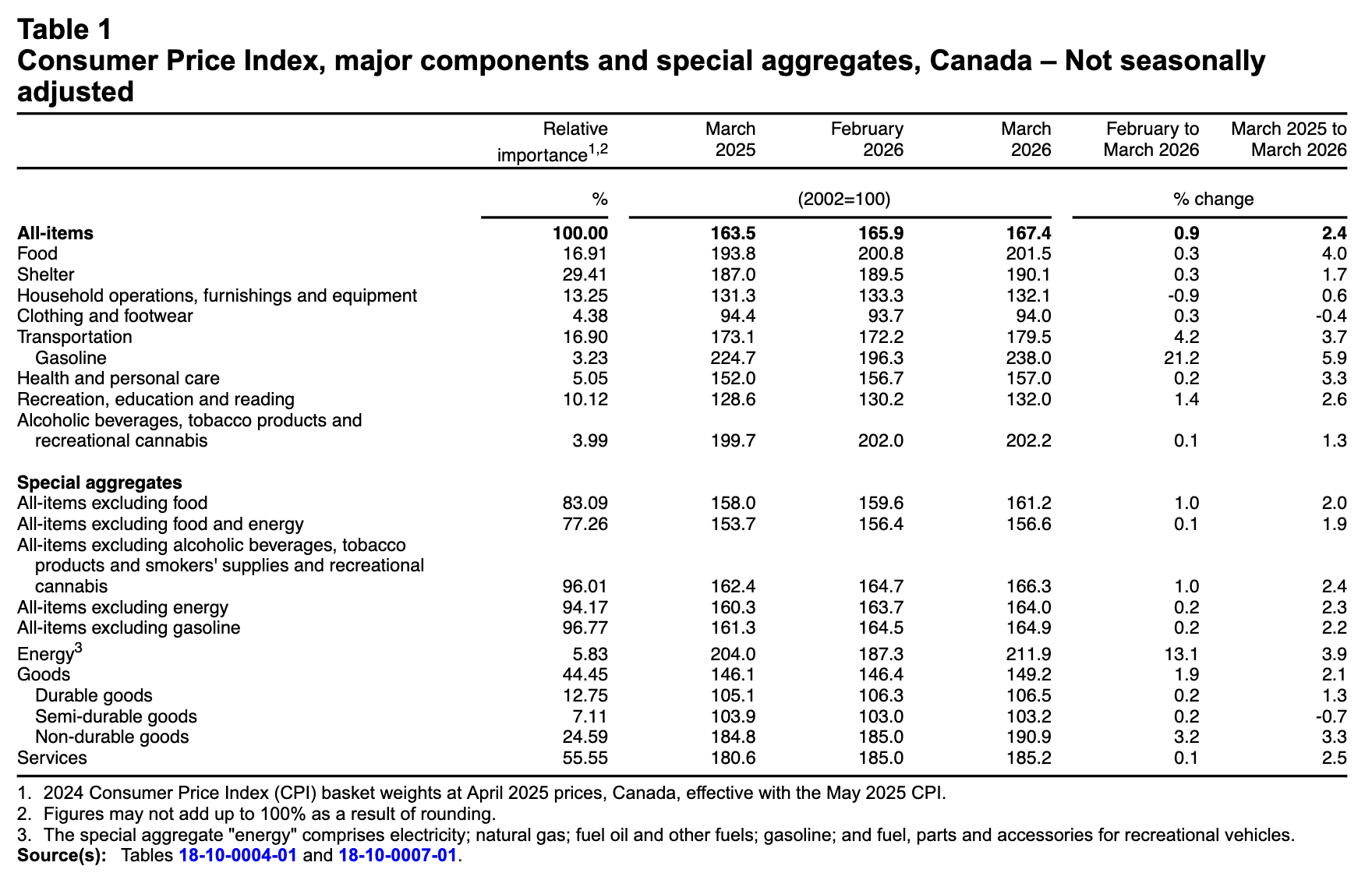

Canada’s consumer price index (CPI) increased by 2.4% year over year (Y-o-Y) in March, up from 1.8% Y-o-Y in February. Statistics Canada (StatsCan) published the data at 8:30 a.m. ET on April 20, 2026, via The Daily report. On a monthly basis, the CPI rose by 0.9%, as the Middle East conflict drove a material increase in energy and gasoline prices.

Despite that, the results were mild relative to expectations. The table below is courtesy of Investing.com. The left column represents March’s figures, while the right column represents forecasters’ consensus estimates. As you can see, there was plenty of red.

Yet, the volatility in commodity prices due to the Middle East conflict has the Bank of Canada (BoC) confronting an uncertain interest rate path. BoC Governor Tiff Macklem said over the weekend that both sides of the dual mandate deserve consideration.

“We’re all feeling like you don’t want to jump too early and raise interest rates and lower growth, particularly when growth is already weak,” Macklem said. “On the other hand, you don’t want to be late and let inflation get a hold and get entrenched.”

As a result, more time, analysis, and judgment are needed to determine the appropriate policy response.

Core CPI

Core measures of the CPI were mixed in March, with the CPI-common index rising to +2.6% (from +2.4%), the CPI-median holding at +2.3% (from +2.3%), and the CPI-trim falling to +2.2% (from +2.3%). These measures exclude the impacts of food and energy, and the BoC places heavy emphasis on core measures because they provide a smoothed distribution of overall inflation.

Please note that food and energy prices are highly volatile and price spikes can occur for reasons outside of the BoC’s control. In contrast, core inflation is mainly driven by consumer demand and gives the BoC a better sense of how the Canadian economy is functioning.

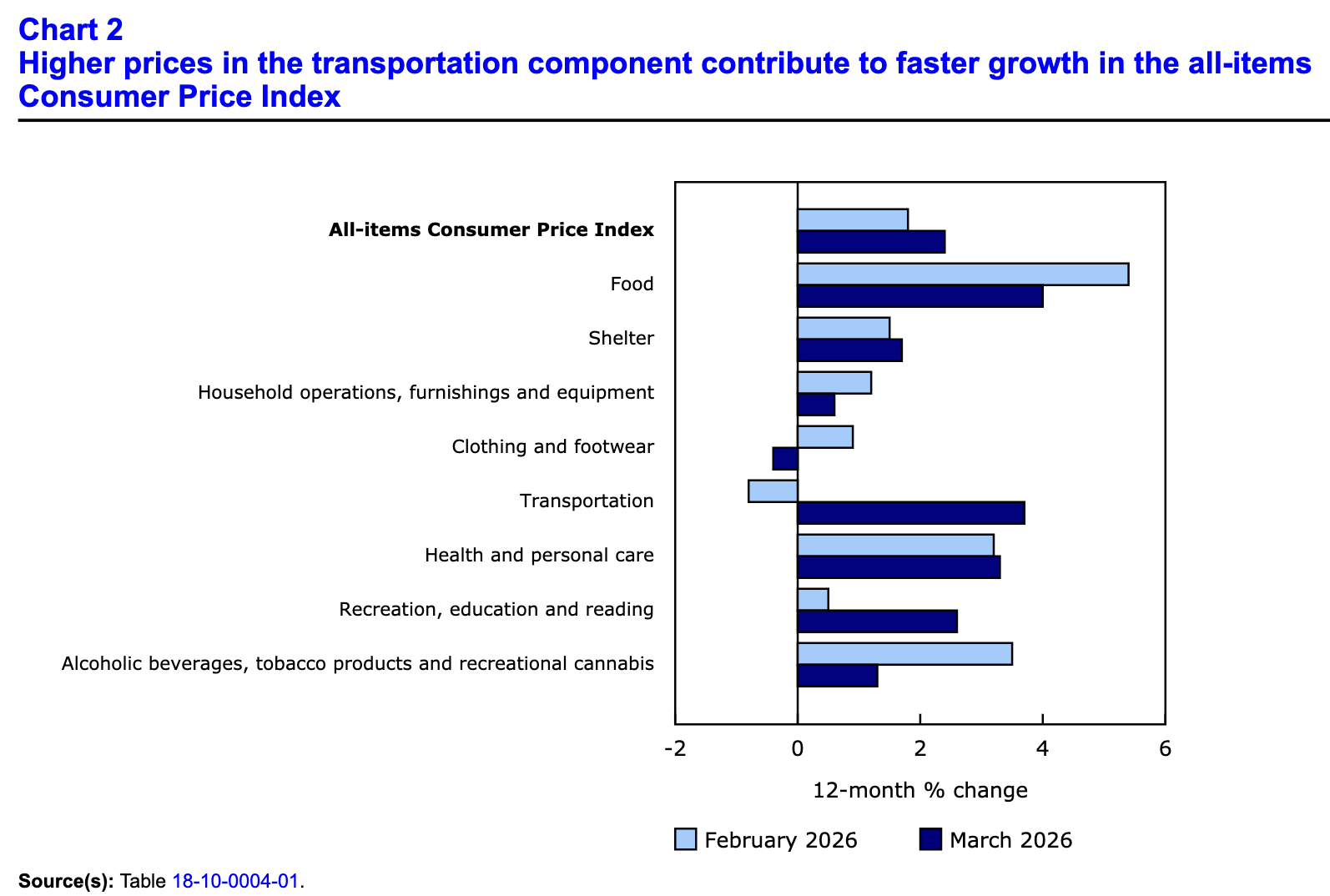

Sector Results

Sector performance was also mixed in March, as food inflation was relatively tame, while transportation showed a noticeable increase. Essentially, energy was the primary culprit. The release stated:

“Higher prices for gasoline were the primary driver of the Y-o-Y acceleration in the CPI, as consumers paid 5.9% more for gasoline in March than they did in the same month the previous year. Prices surged 21.2% on a monthly basis, the largest price increase for gasoline on record, due to the supply shock resulting from the conflict in the Middle East.”

For context, the eight sectors include food, shelter, household operations, furnishings and equipment, clothing and footwear, transportation, health and personal care items, recreation and education expenses, and alcohol and tobacco products.

Food Inflation

While consolidated food inflation decreased Y-o-Y, food purchased from stores rose by 4.4% in March versus 4.1% in February. Fresh vegetables jumped by 7.8% (the largest increase since rising by 8.7% in August 2023), while cucumbers, peppers, and celery had notable price growth due in part to supply constraints from adverse growing conditions in producing countries.

More Uncertainty

While Macklem added that “We’re not surprised and we’re not even that worried if we see near-term inflation expectations going up,” ensuring another post-COVID inflationary spiral doesn’t occur is top of mind. However, with the demand backdrop much different now than it was then, the BoC should feel comfortable looking through the oil volatility.

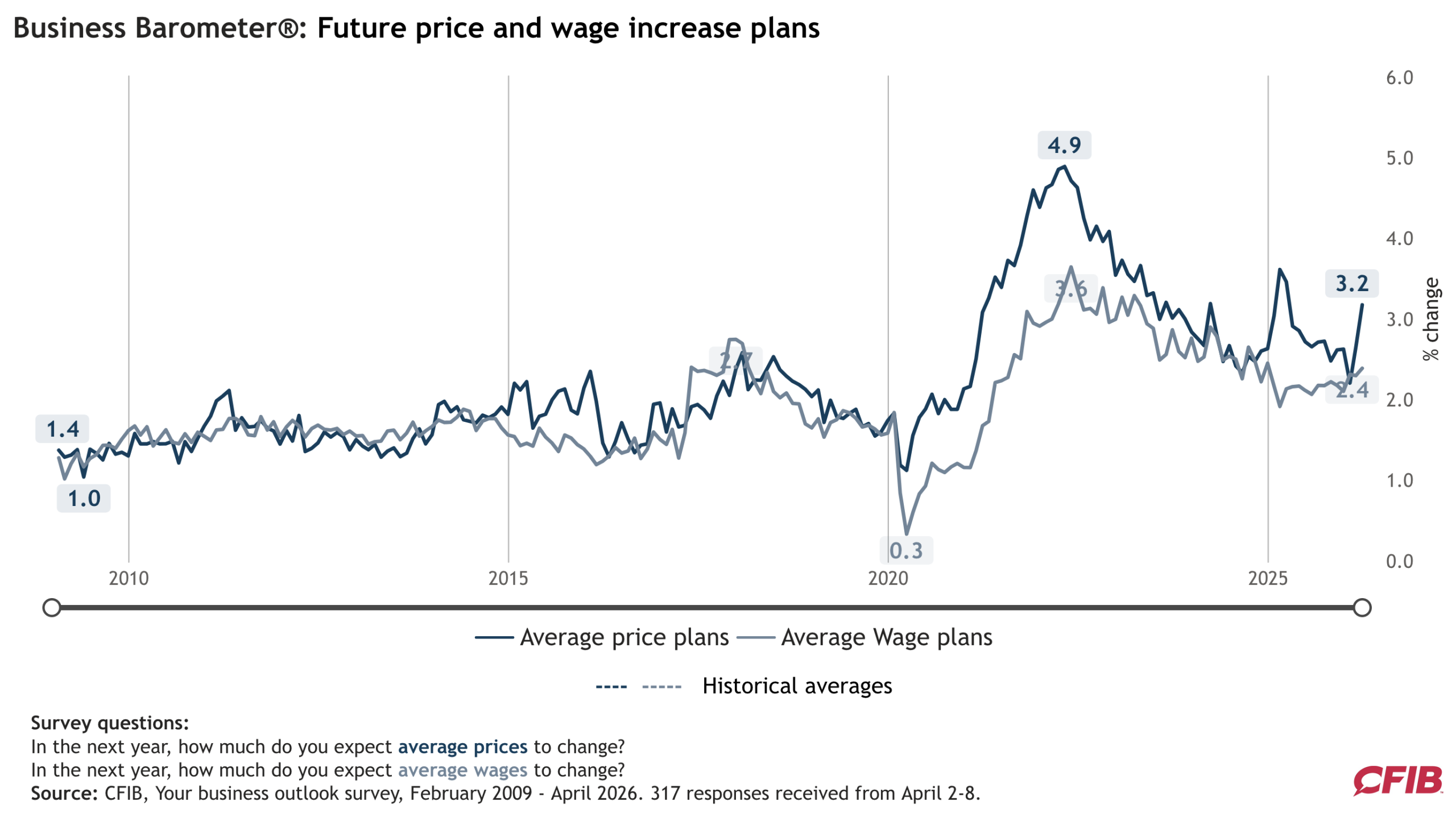

For example, the Canadian Federation of Independent Business (CFIB) released its latest Monthly Business Barometer on Apr. 16. It tracks the confidence and expectations of Canadian small businesses.

The report noted how “The average price increase jumped up to 3.2% in April, marking the highest monthly change since the tariff war last March.” In contrast, “the average wage increase increased slightly to 2.4%, the first notable shift after roughly 12 months of readings clustered around the 2.2% mark.”

In a nutshell: with wages still underperforming and largely stagnant, consumers will have trouble stimulating demand like in 2021/2022 if wages don’t keep pace with price increases.

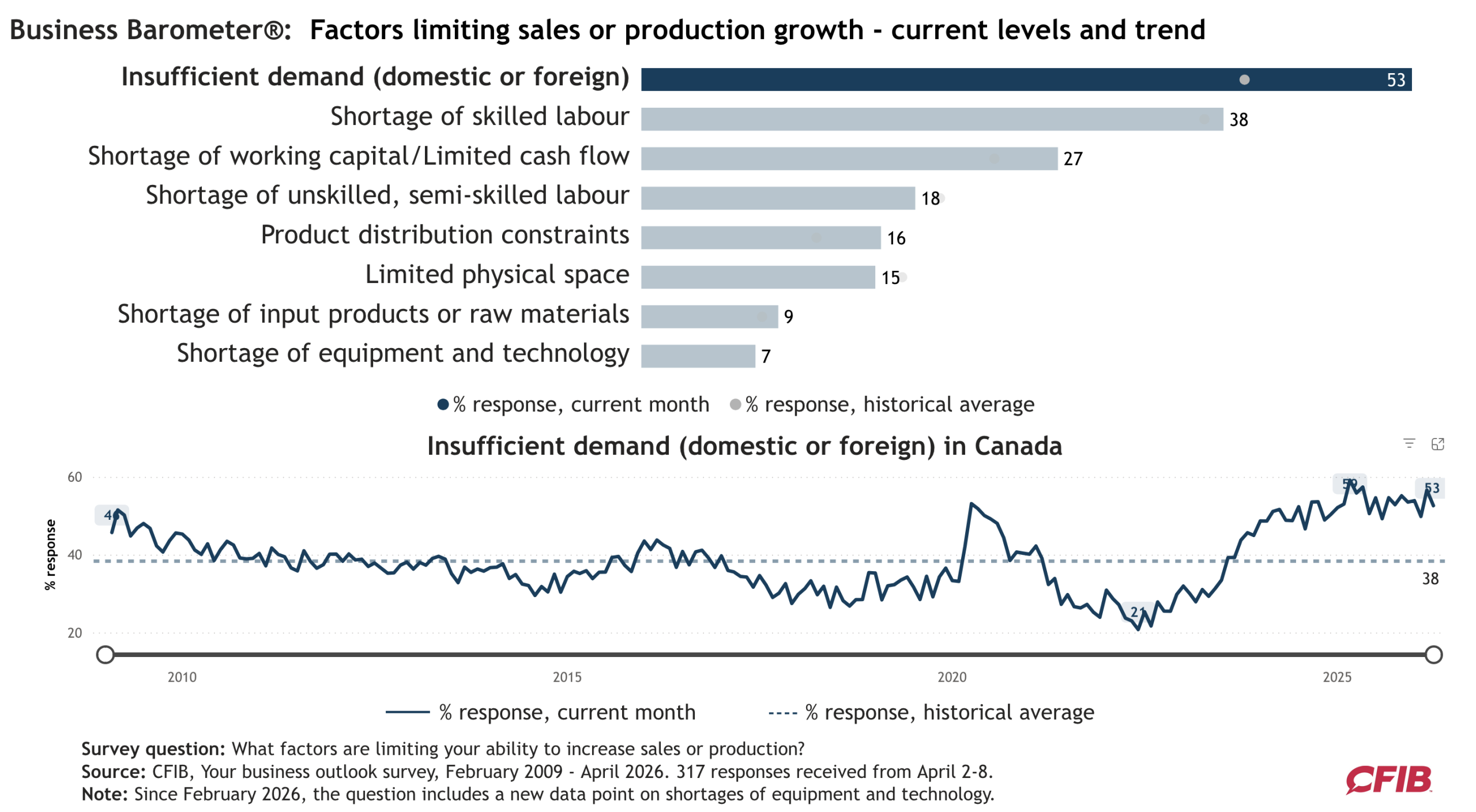

To that point, the report added: “Insufficient demand remains the top constraint to business and production expansion as indicated by 53% of SMEs — still a very high level for the indicator.”

For context, the long-run average is 38%, and the metric hit a series low in 2022. Yet, now the metric is closer to a series high, and highlights how weak demand is unlikely to incite the kind of buying spree that unleashed inflation following the pandemic.

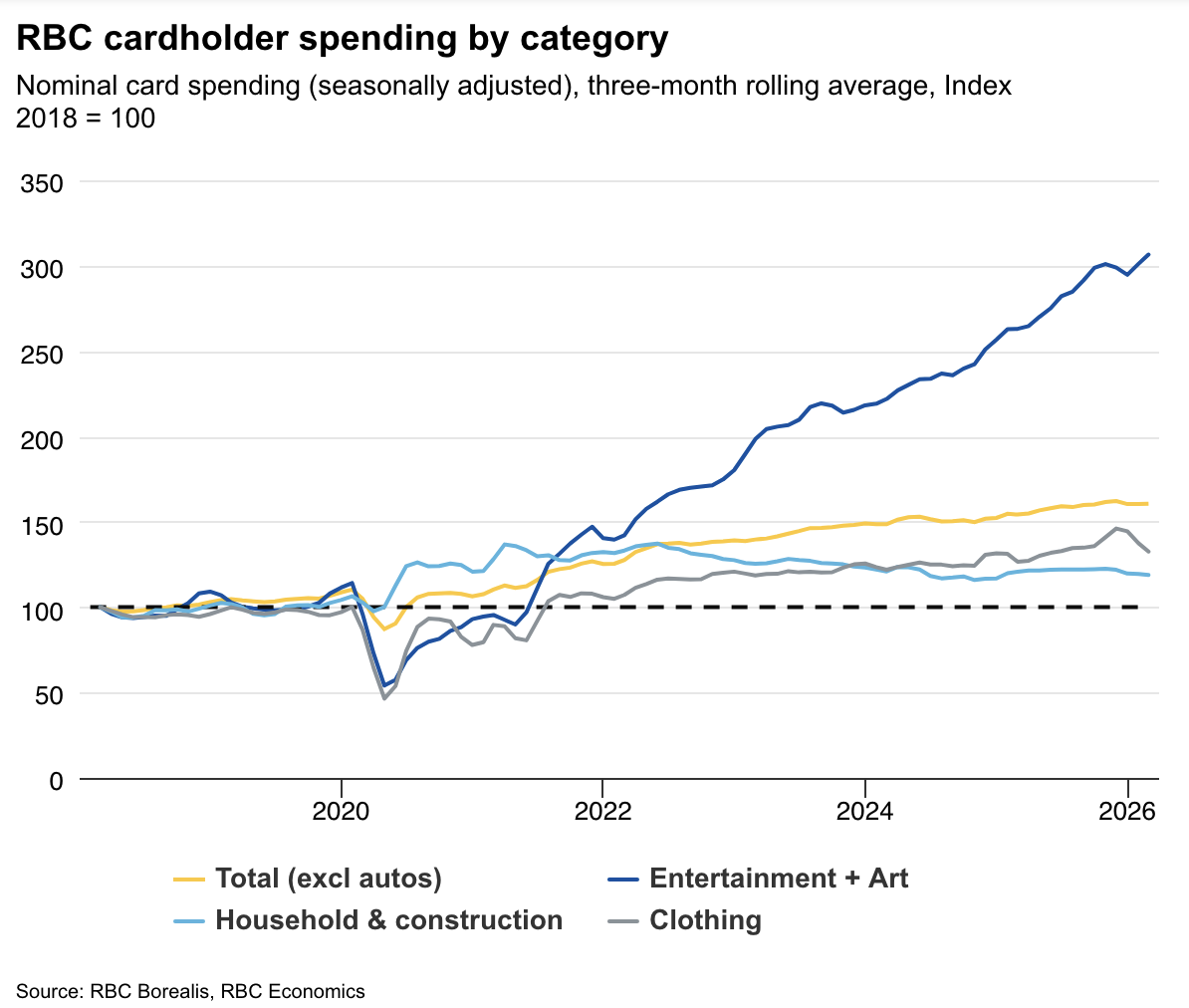

Finally, RBC Economics noted on Apr. 15 that Canadian cardholder spending remains tepid as consumers pull back on discretionary purchases. The release stated:

“A sharp increase in gasoline prices, tied to geopolitical tensions, boosted spending at fuel stations, and contributed to strength in essentials’ purchases… Excluding gasoline, spending still rose in March, but slowed from February, remaining weak on a three-month average.”

Thus, while some categories have shown strength, total cardholder spending (the yellow line below) has mostly flatlined and remains below its December 2025 high. Consequently, it will likely take a material increase in Canadians’ spending activity to spur another round of long-lasting inflation.

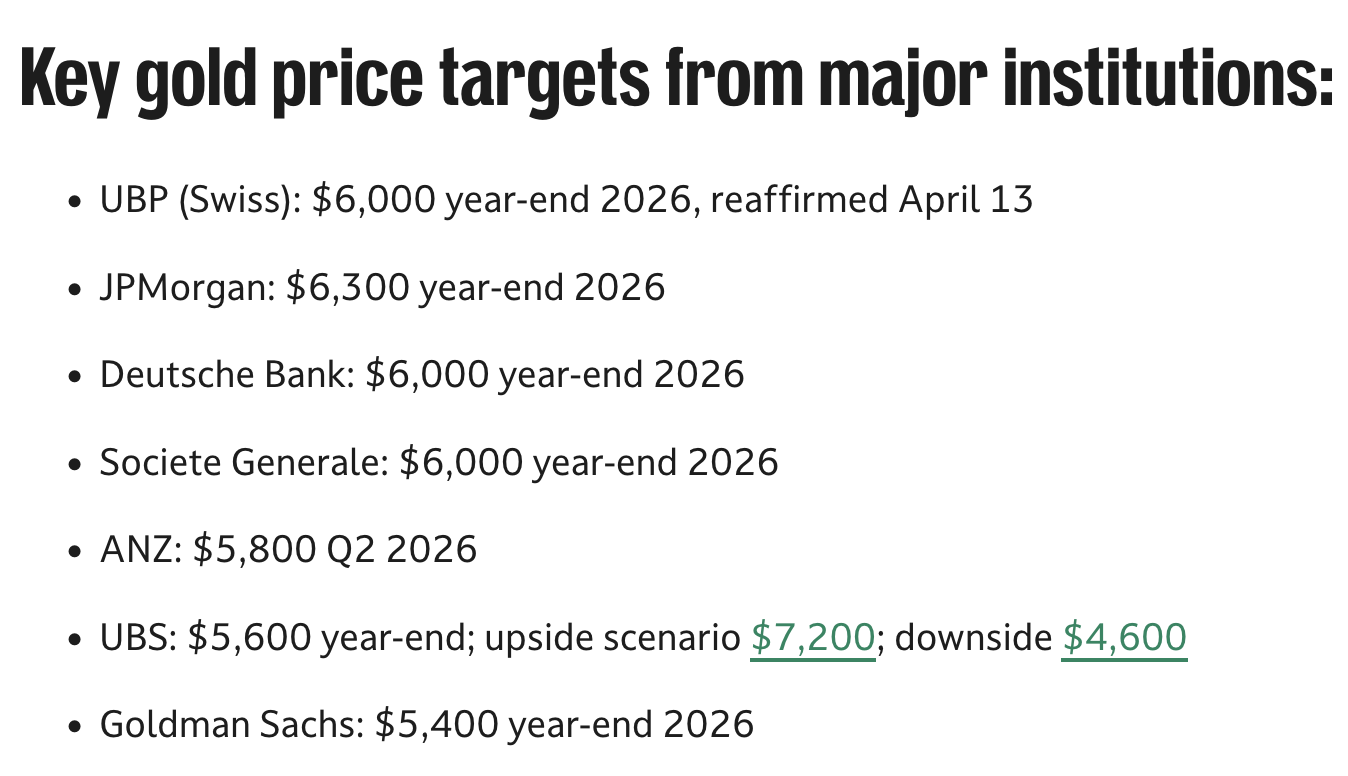

Turning to the financial markets, volatility should remain as investors weigh the uncertain economic impact of the war and higher commodities prices. However, major institutions are bullish on gold and expect the yellow metal to rally sharply into year-end.

TheStreet compiled the list below on Apr. 14, and the price targets show how most of Wall Street remains optimistic about gold’s future performance.

Dedicating a small portion of one’s TFSA or RRSP portfolio to precious metals may help mitigate some of the geopolitical risks and negative effects of inflation. If you want to get started with investing in metals such as gold and silver, read our free guide to gold buying in Canada in 2026 today.

In addition, if higher interest rates and mounting credit card debt have become a financial burden, several solutions can be tailored to your income, credit score, debt level, and interactions with creditors. For more information, our extensive guide has management solutions for credit card borrowers at all debt levels.

Similarly, while bankruptcy can help under the right circumstances, there are seven alternatives to consider before filing. Not every option fits every person, and by weighing the pros and cons of each, you can find the right fit for you.

For hands-on help, speaking with a professional is often wise. Several for-profit and non-profit counselling and debt management firms can help explain the process, outcomes, and payment solutions that best fit your unique circumstances. Farber Debt Solutions meets this criterion. It’s a Licensed Insolvency Trustee that assists Canadians with credit counselling, consumer proposals, personal bankruptcies, and other serious debt problems that often require legal assistance.

For additional resources, please consult our list of reliable lenders to see a wide range of products and services available in your area.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.