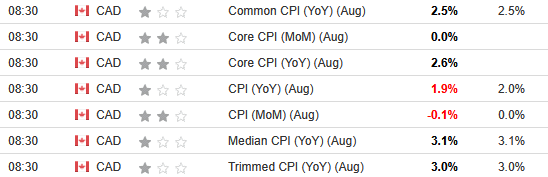

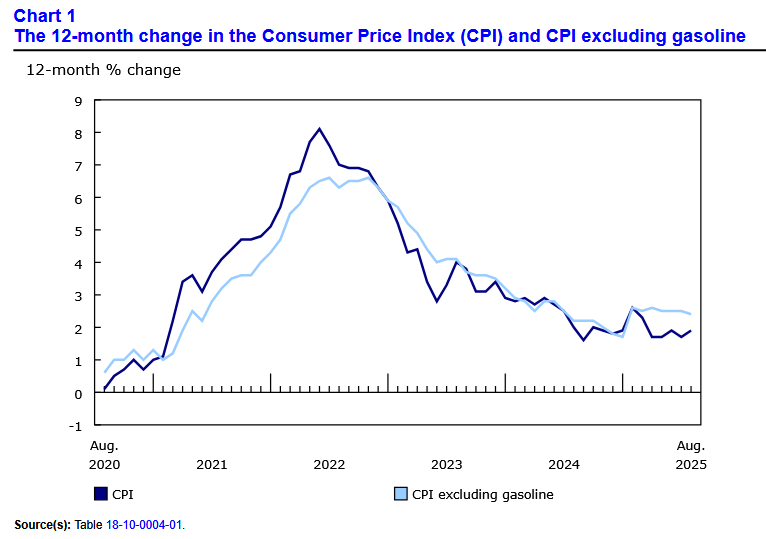

Canada’s consumer price index (CPI) increased by 1.9% year over year (Y-o-Y) in August, up from 1.7% Y-o-Y in July. Statistics Canada (StatsCan) published the data at 8:30 a.m. ET on September 16, 2025, via The Daily report. On a monthly basis, the CPI fell by 0.1%, and most metrics aligned with economists’ consensus estimates.

The table below is courtesy of Investing.com. The left column represents August’s figures, while the right column represents forecasters’ expectations. As you can see, the headline CPI missed the mark MoM and Y-o-Y, as the impact of tariffs continues to hurt growth more than it helps inflation.

To that point, the Bank of Canada (BoC) will likely cut interest rates at tomorrow’s meeting. GDP growth has been flat, inflation remains somewhat weak, the labour market has slowed, and housing has declined. The troubling combination should warrant further policy easing; otherwise, the BoC may not meet its growth and unemployment estimates.

Steady Core CPI

Core measures of the CPI were well behaved again in August, with the CPI-common index falling to +2.5% (from +2.6%), while the CPI-median held at +3.1% (from +3.1%), and the CPI-trim declined to +3.0% (from +3.1%). These measures exclude the impacts of food and energy, and the BoC places heavy emphasis on core measures because they provide a smoothed distribution of overall inflation.

Please note that food and energy prices are highly volatile and price spikes can occur for reasons outside of the BoC’s control. In contrast, core inflation is mainly driven by consumer demand and gives the BoC a better sense of how the Canadian economy is functioning.

Sector Results

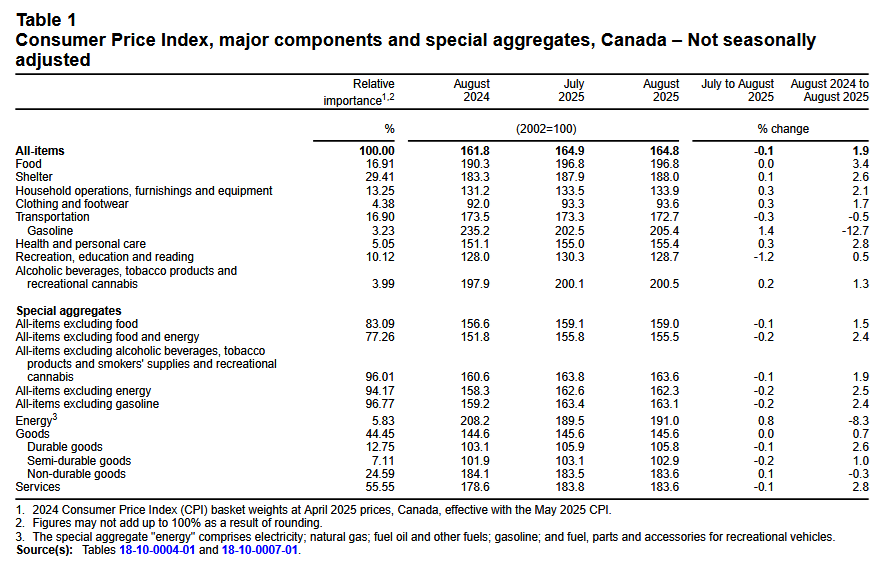

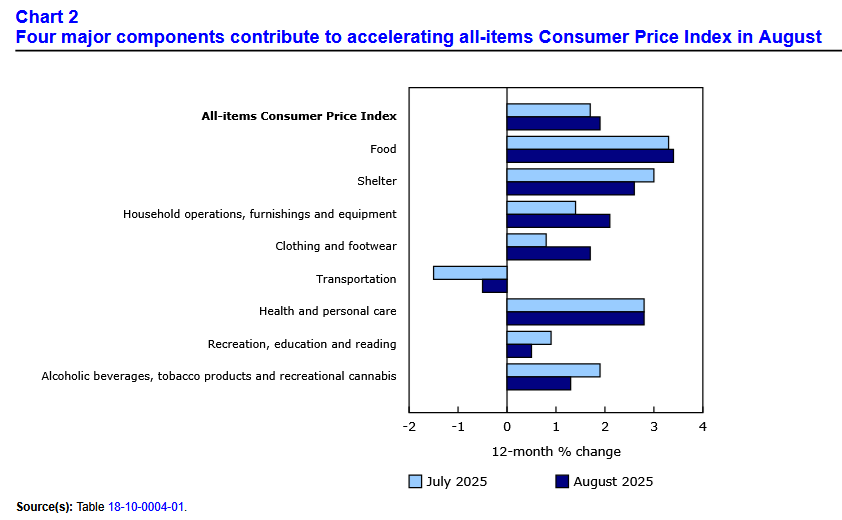

Four major sectors recorded Y-o-Y increases in August, with food, household items, and clothing outperforming, while transportation remained in deflation.

For context, the eight sectors include food, shelter, household operations, furnishings and equipment, clothing and footwear, transportation, health and personal care items, recreation and education expenses, and alcohol and tobacco products.

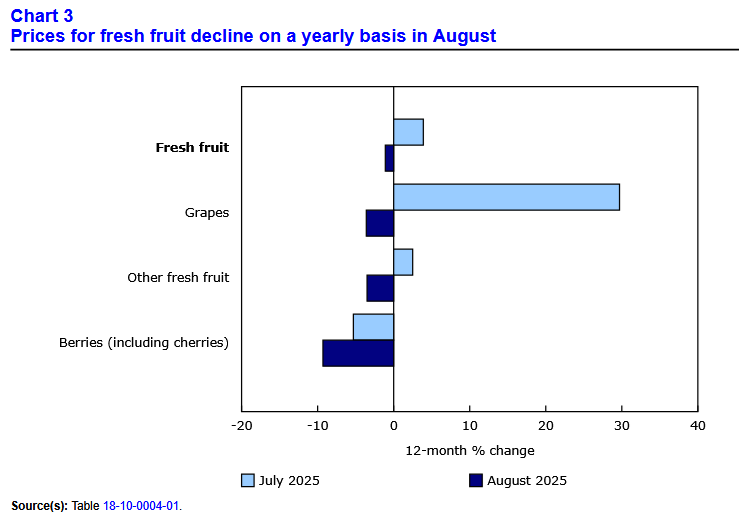

Grocery Inflation Slows

Grocery inflation was flat MoM in August and remained near 3.4% Y-o-Y (not seasonally adjusted). Fresh or frozen beef (+12.7%) and processed meat (+5.3%) put upward pressure on the index, while fresh fruit fell by 1.1%, with grapes, other fresh fruit, and berries driving the deceleration.

Lower Rates Ahead?

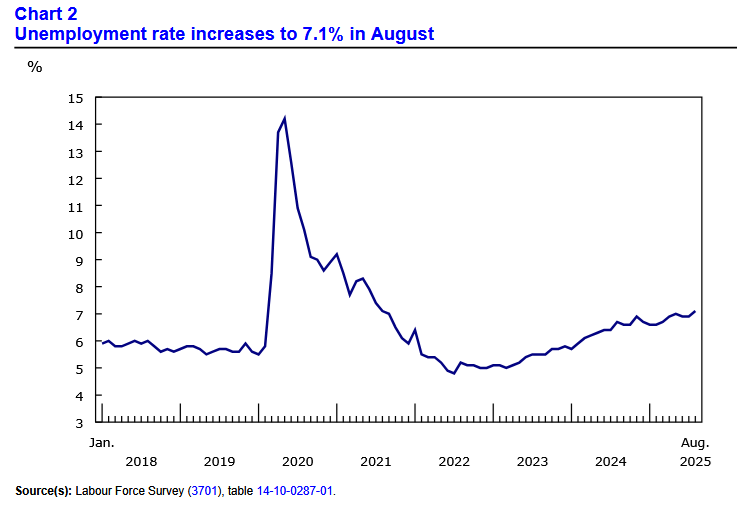

The Canadian labour market continues to deteriorate, and the slowdown should prompt a response from the BoC in the months ahead. For example, Statistics Canada noted on Sep. 5:

“Employment declined by 66,000 (-0.3%) in August, largely the result of a decline in part-time work, and the employment rate fell 0.2 percentage points to 60.5%. The unemployment rate rose 0.2 percentage points to 7.1%.

“Employment fell for core-aged (25 to 54 years old) men (-58,000; -0.8%) and core-aged women (-35,000; -0.5%) in August. There was little change in employment for youth aged 15 to 24 and people aged 55 and older.”

Thus, while seasonal layoffs are often the culprit as students head back to school in September, the concentration in core-aged (25 to 54 years old) Canadians signals the decrease was driven by prime-age workers. As a result, with the overall unemployment rate hitting a new cycle high of 7.1%, the BoC may look to loosen monetary policy tomorrow.

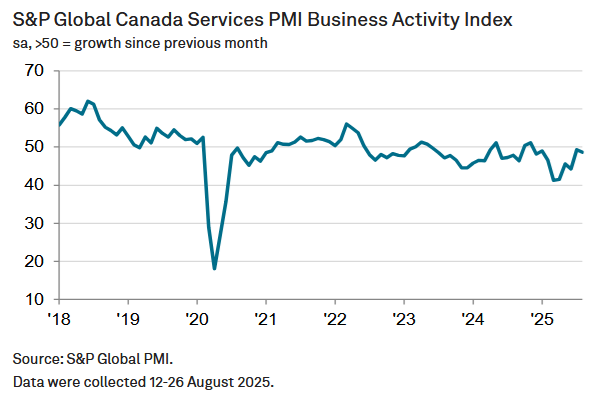

Also noteworthy, S&P Global revealed on Sep. 4 that Canada’s service sector activity continued its decline, as “market conditions remained unfavourable, characterised by uncertainty caused by tariffs. Business confidence also moderated and remained well below trend.”

The report added:

“For the ninth successive month, a net fall in private sector output was recorded. This was highlighted by the S&P Global Canada Composite PMI Output Index* which recorded 48.4 in August. That was down from 48.7 in July and reflected concurrent contractions of output in the manufacturing and service sectors.

“The downturn in overall activity reflected reduced private sector sales, also for a ninth month running. Confidence in the outlook remained historically subdued but employment numbers were stable, enabling firms to comfortably keep on top of workloads.”

So, with the Canadian economy operating near stall speed, the troubling data may warrant further action from the BoC to help stimulate consumer demand and employment.

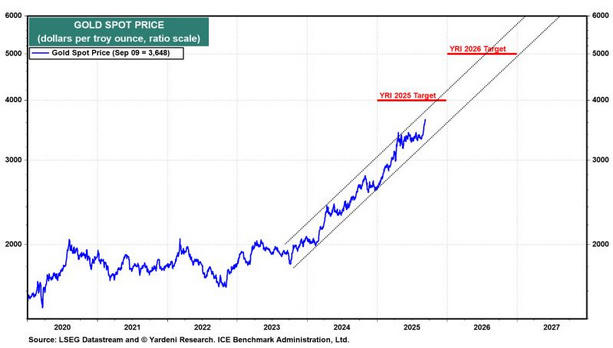

Yet, while inflation and recession uncertainty spread across North America, and geopolitical tensions provide a global tailwind, gold has been a noticeable outperformer. And while the epic run could result in a short-term correction, Ed Yardeni expects the yellow metal to hit $4,000 by the end of 2025 and $5,000 by the end of 2026. Consequently, the recent bull market could have plenty of room to run.

Dedicating a small portion of one’s TFSA or RRSP portfolio to precious metals may help mitigate some of the geopolitical risks and negative effects of inflation. If you want to get started with investing in metals such as gold and silver, read our free guide to gold buying in Canada in 2024 today.

In addition, if financial concerns are keeping you up at night, Consolidated Credit Canada helps create debt management plans and negotiates with creditors on your behalf. The group is recognized by organizations like the Canadian Association of Credit Counselling Services and has an A+ rating with the Better Business Bureau. Moreover, the team can also assist with budgeting, housing counseling, student loan advice, and financial education.

Similarly, Fig Financial is an excellent resource for debt consolidation, as the firm provides unsecured personal loans from $2,000 to $35,000, terms from 24 to 84 months, and APRs from 8.99% to 29.49%.

For DIY and large durable goods, LendCare is a trusted resource for financing auto, powersports, home improvement, healthcare (dental, vision, cosmetic), and general retail purchases. Loans commonly range from $500 to $15,000, and there are typically no prepayment penalties.

Finally, Merchant Growth is great for business owners looking to expand their operations or enter new markets. The company provides term loans, lines of credit, and merchant cash advances, and unsecured financing means you don’t have to post collateral and risk losing your asset. The only catch is that your company must be in business for at least six months with $10,000 per month or more in sales.

For additional resources, please consult our list of reputable lenders to see the best products and services available in your area.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.