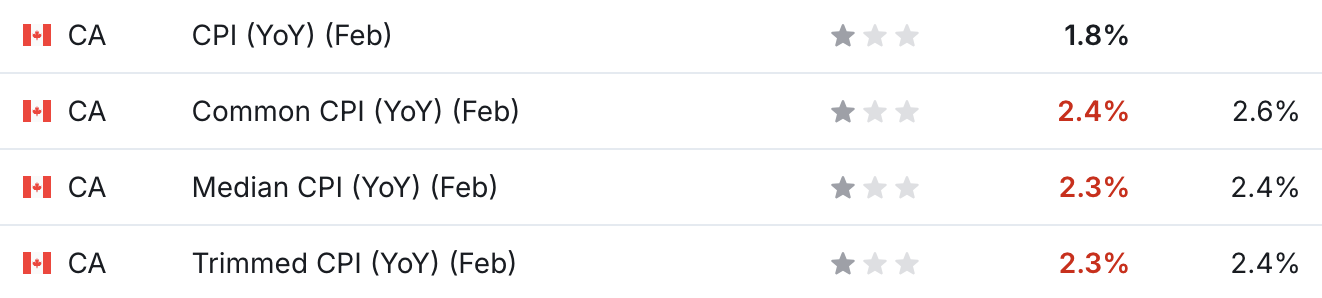

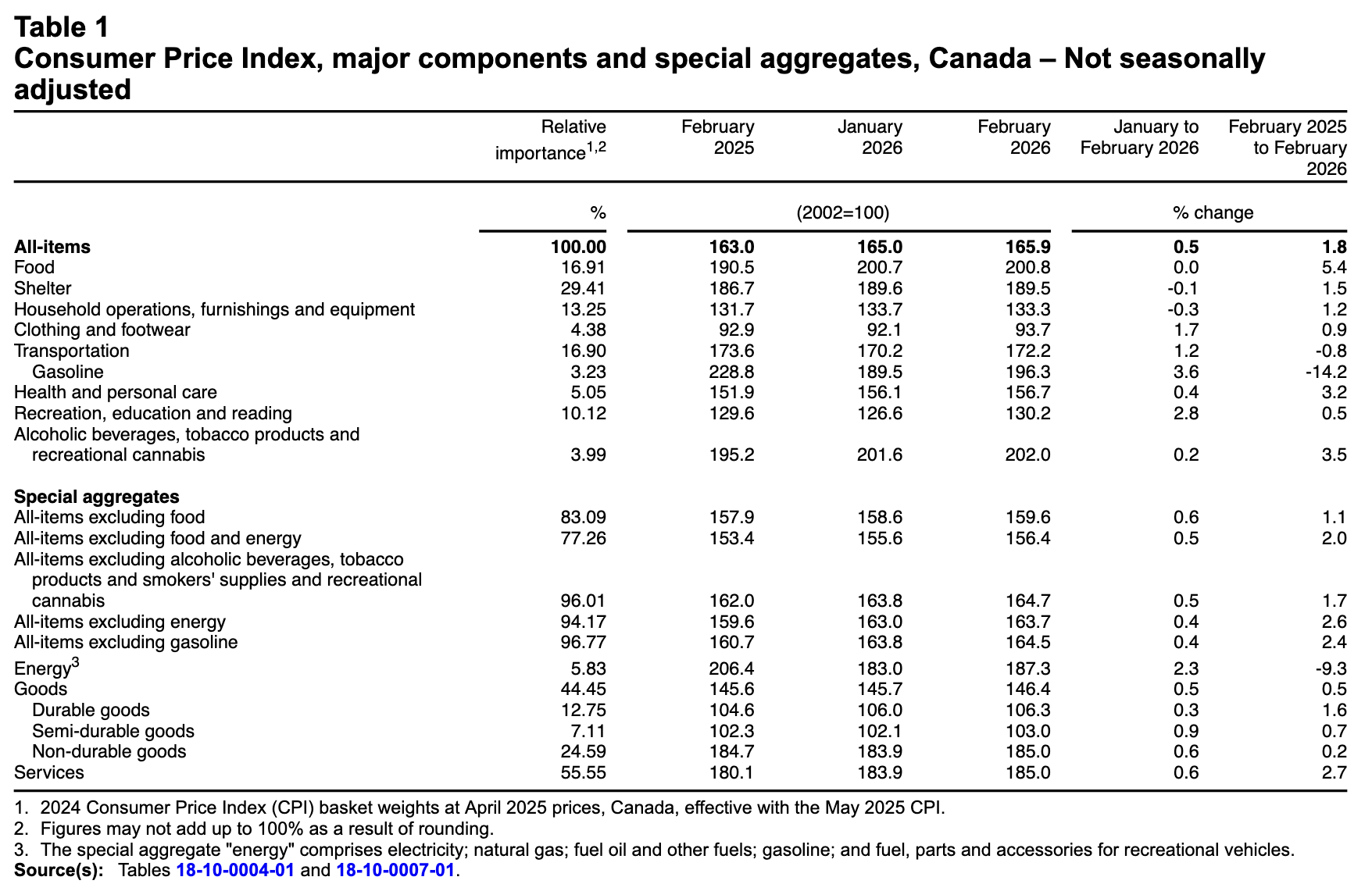

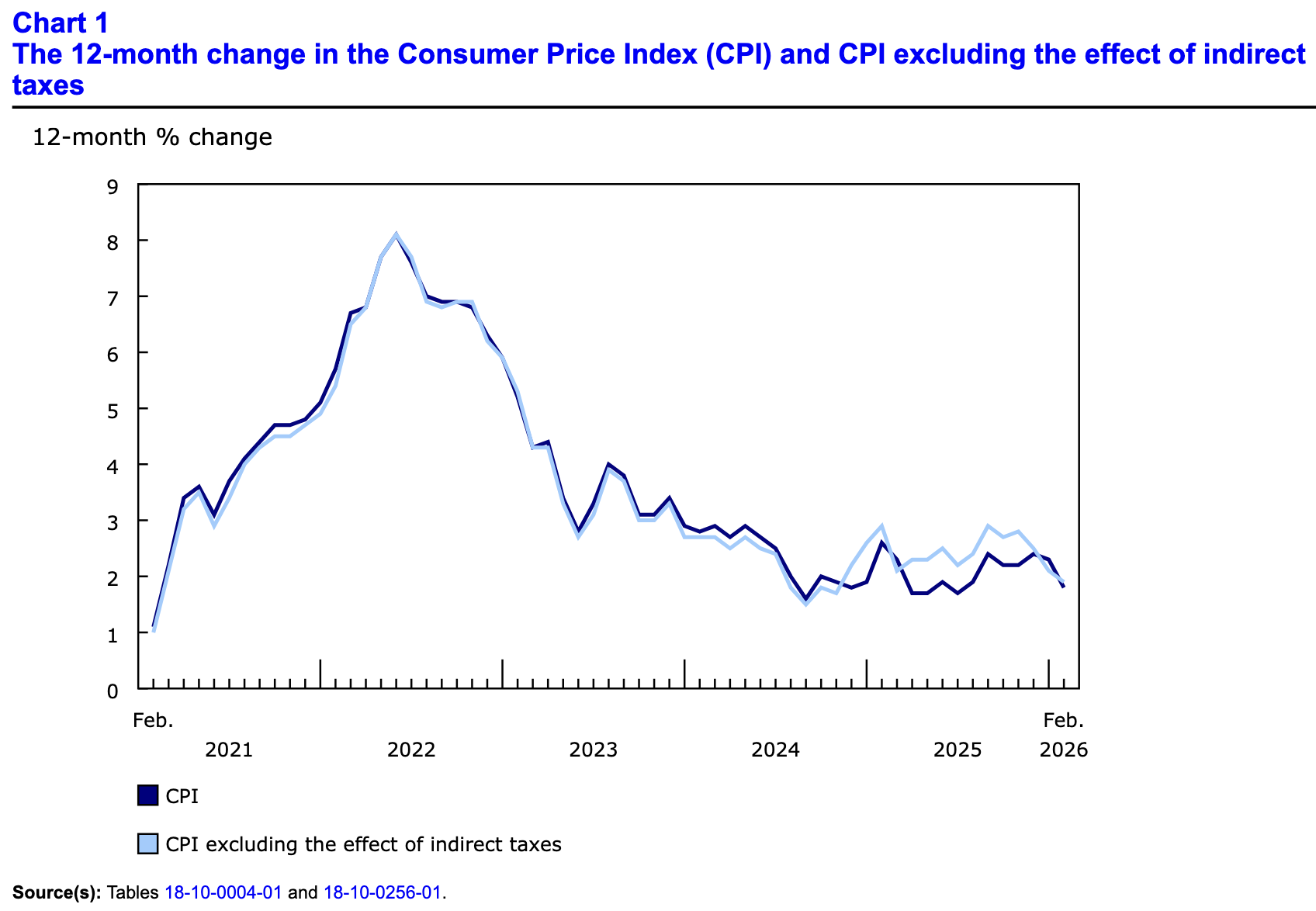

Canada’s consumer price index (CPI) increased by 1.8% year over year (Y-o-Y) in February, down from 2.3% Y-o-Y in January. Statistics Canada (StatsCan) published the data at 8:30 a.m. ET on March 16, 2026, via The Daily report. On a monthly basis, the CPI rose by 0.5%, and base effects from last year’s GST/HST holiday provided some distortions that helped slow the Y-o-Y figure.

Overall, the soft results largely missed expectations. The table below is courtesy of Investing.com. The left column represents February’s figures, while the right column represents forecasters’ consensus estimates. As you can see, the core metrics were subdued.

Although, as the Bank of Canada (BoC) confronts the Middle East conflict and the prospect of higher-for-longer oil prices, managing its dual mandate will require more of a proactive, and less reactive, approach. For example, traders are pricing in a rate hike by the end of the year, as higher crude prices could stimulate inflation. However, if employment suffers along the way, the BoC will face some tough choices over the next few months.

Core CPI

Core measures of the CPI all slowed in February, with the CPI-common index falling to +2.4% (from +2.7%), the CPI-median falling to +2.3% (from +2.5%), and the CPI-trim falling to +2.3% (from +2.4%). These measures exclude the impacts of food and energy, and the BoC places heavy emphasis on core measures because they provide a smoothed distribution of overall inflation.

Please note that food and energy prices are highly volatile and price spikes can occur for reasons outside of the BoC’s control. In contrast, core inflation is mainly driven by consumer demand and gives the BoC a better sense of how the Canadian economy is functioning.

Sector Results

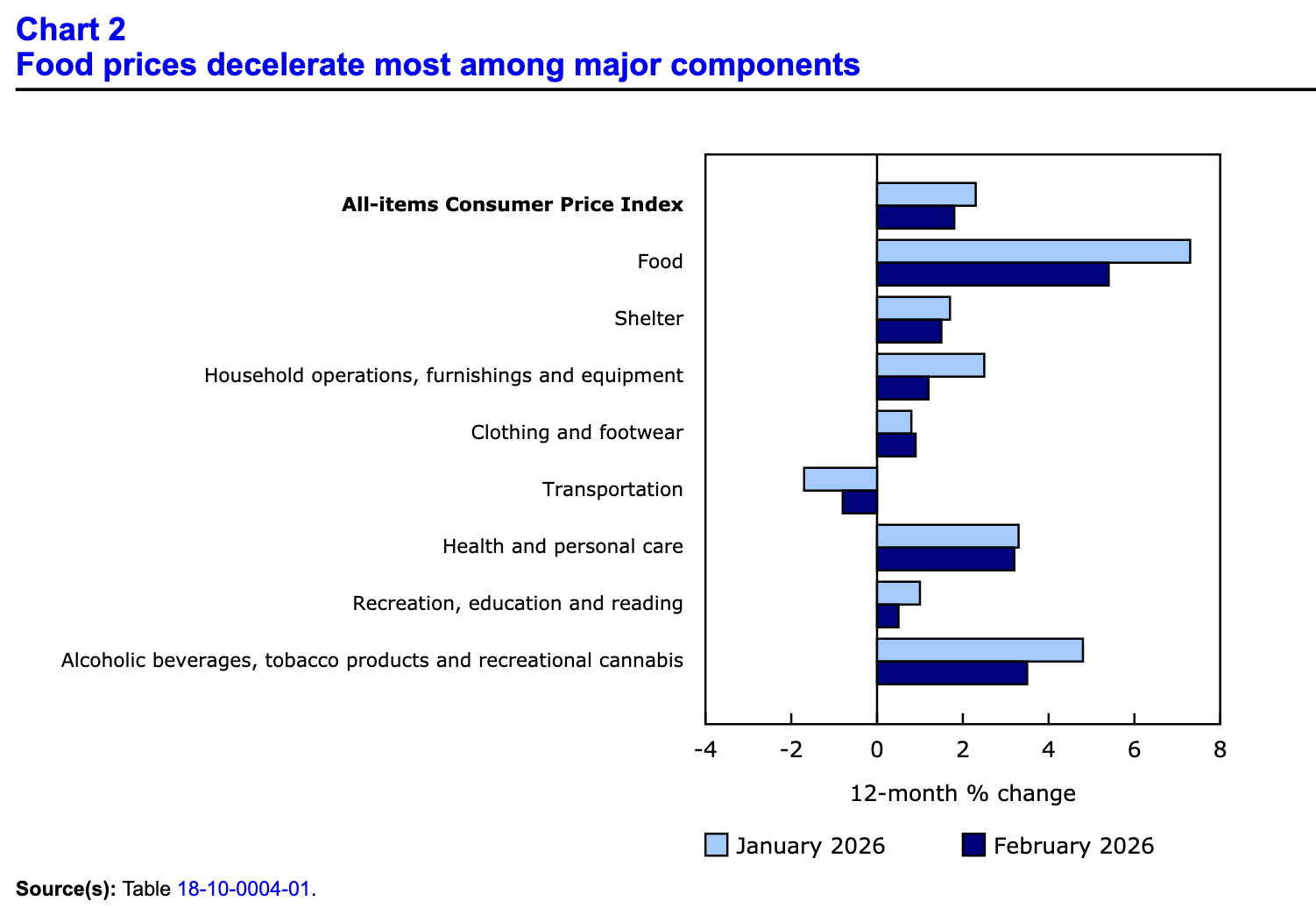

Sector performance also slowed in February, as nearly every category declined Y-o-Y relative to January. However, base effects from the GST/HST holiday were meaningful once again. The report noted:

“The end of the GST/HST break on February 15, 2025, resulted in monthly price increases for affected products in that month…. This put downward pressure on year-over-year price growth for alcoholic beverages purchased from stores (+5.6%), toys, games (excluding video games) and hobby supplies (+5.4%), and alcoholic beverages served in licensed establishments (+6.8%).”

For context, the eight sectors include food, shelter, household operations, furnishings and equipment, clothing and footwear, transportation, health and personal care items, recreation and education expenses, and alcohol and tobacco products.

Food Inflation

Grocery inflation slowed from 4.8% Y-o-Y in January to 4.1% Y-o-Y in February, and the deceleration was led by prices for fresh or frozen beef, which dipped from an 18.8% annual increase in January to a 13.9% rise in February.

Yet, while “growth in grocery prices slowed in February, they have risen 30.1% since February 2021.”

Bad Combination

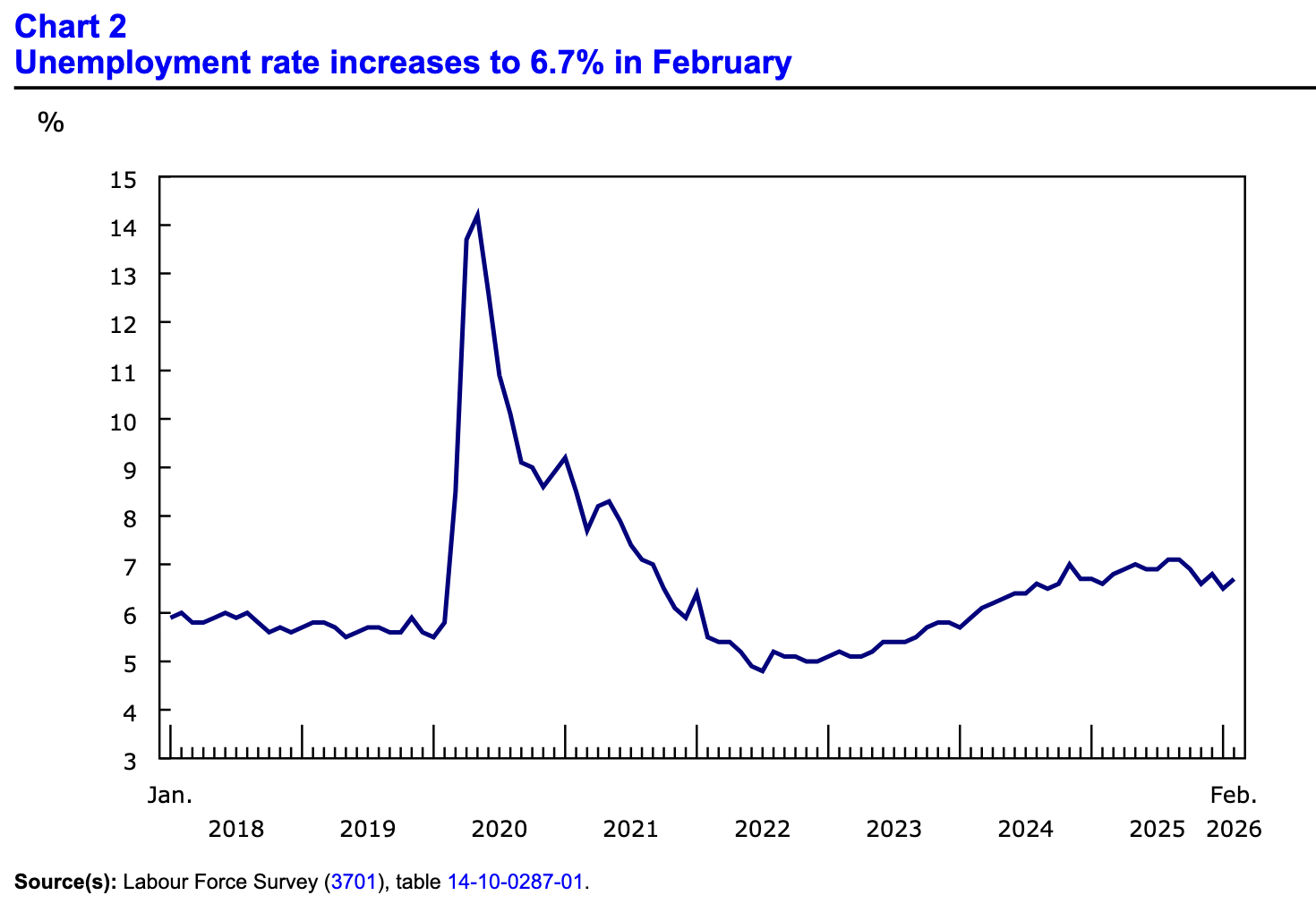

The BoC had been in a comfortable position, with employment remaining buoyant while inflation trended lower. Fast forward two months, and the outlook has flipped.

For example, Statistics Canada revealed on Mar. 13 that “Employment declined by 84,000 (-0.4%) in February, after edging down in January (-25,000; -0.1%). These cumulative declines partially offset the upward trend observed in the fall of 2025.” Moreover, “the number of people working full-time declined by 108,000 (-0.6%), offsetting growth recorded over the previous two months.”

Add it all up, and BMO Chief Economist Doug Porter said, “No sense sugarcoating this one—this is simply a brutal result, and the near absence of net job growth in the past year is perhaps the most telling reading here. … Somehow, the market continues to price in Bank of Canada rate hikes for later this year, but if this employment report is at all indicative of underlying economic conditions, the last thing the Bank would be considering would be rate hikes.”

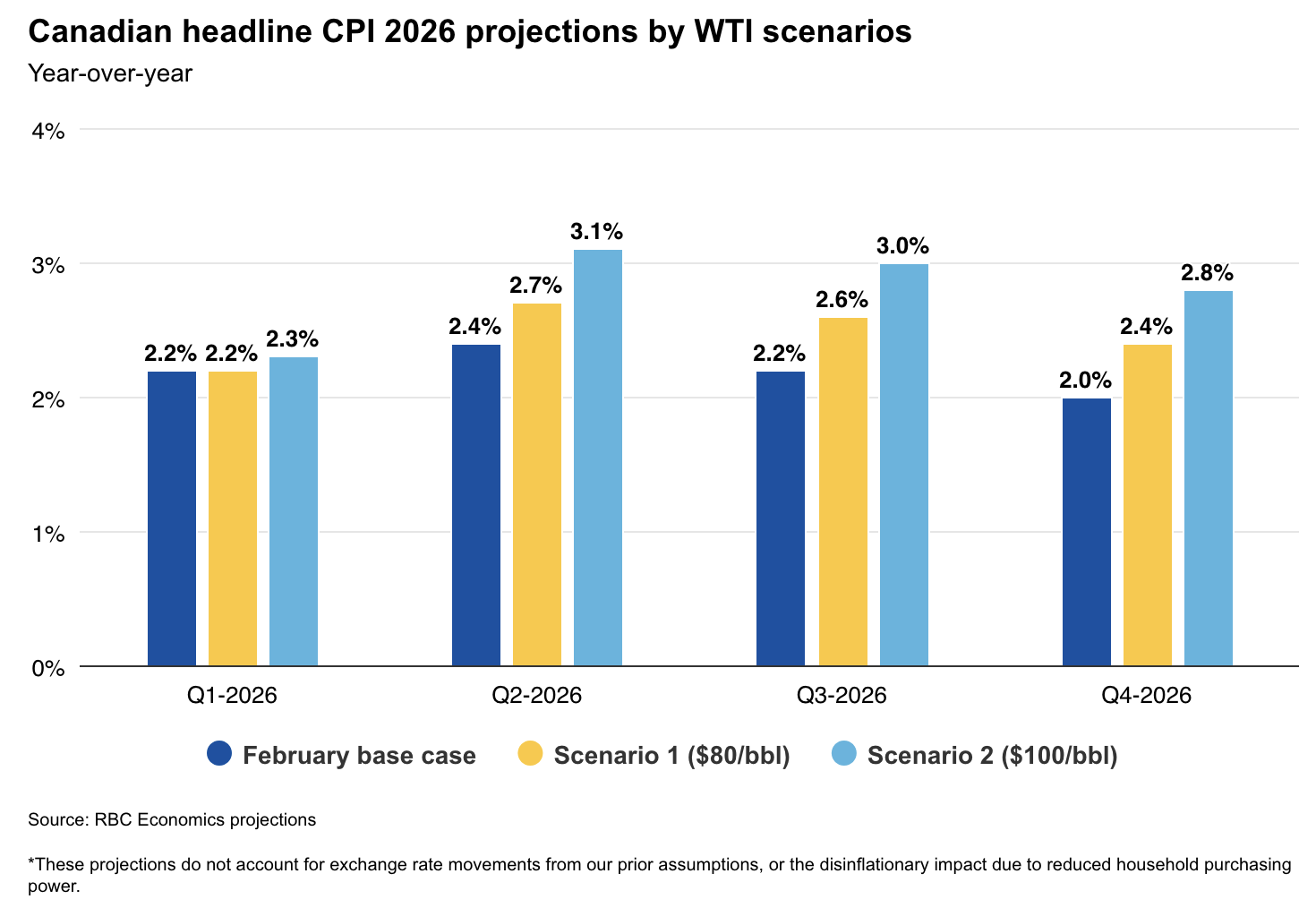

From the other perspective, data from RBC Economics highlights how the “crude calculations” may not be as troublesome as the narrative suggests.

To explain, the bank’s base case is a short-term conflict where oil prices normalize and have a minimal impact on the headline CPI (the dark blue bars). However, under scenarios of $80 and $100 WTI (the yellow and light blue bars), the headline CPI peaks near 3% and then resumes its descent later in 2026.

Also, the analysis doesn’t assume a demand decline due to households’ reduced consumption capacity, which could help reduce inflation in other categories. Consequently, a rate hike seems like an overreaction to a short-term supply disruption.

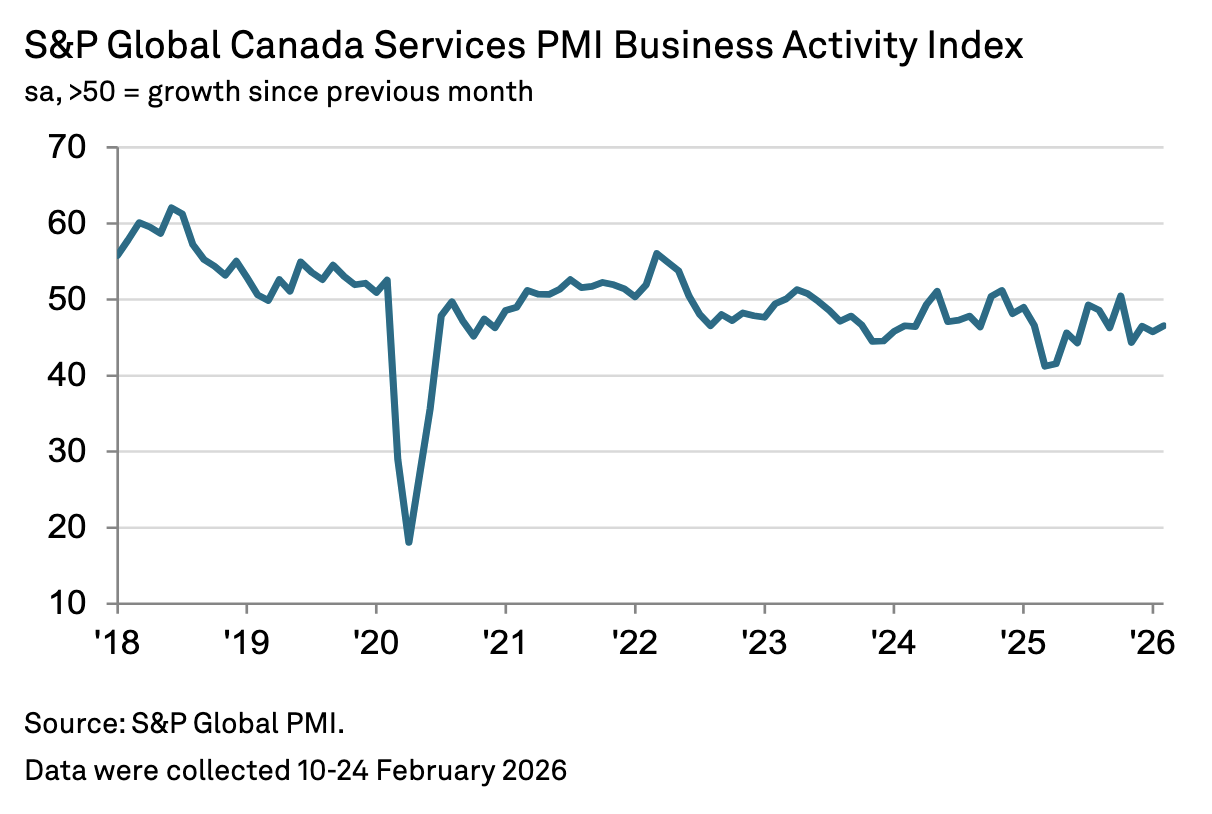

As another indicator, roughly 70% of Canadian GDP growth is driven by services. And S&P Global noted on Mar. 4 that “Canada’s service sector remained in a downturn during February, with activity and new business falling again amid reports of a difficult trading environment. Firms subsequently reported further cuts to their employment numbers by not replacing leavers or enacting forced layoffs. More positive, however, was an uplift in confidence to its highest level since last October. Moreover, cost inflation softened to its lowest level since September 2024.”

Paul Smith, Economics Director at S&P Global Market Intelligence, added:

“The weakness in activity and the labour market was also accompanied by a further softening of cost inflation. Falling to its lowest level since September 2024, the downturn in cost inflation therefore adds to the ‘dovish’ nature of this month’s report and pushes the door ajar for further rate cuts from the Bank of Canada in 2026.”

Thus, while traders seem intent on a BoC rate hike, the data suggest a different outcome.

Turning to the financial markets, gold has been on a wild ride as traders digest geopolitics, credit concerns, and overbought technical conditions. But despite that, Dr. Ed Yardeni told Bloomberg on Mar. 10 that he expects gold to hit $6,000 by the end of 2026 and $10,000 by the end of the decade. Consequently, patient bulls could be rewarded over the long term.

Dedicating a small portion of one’s TFSA or RRSP portfolio to precious metals may help mitigate some of the geopolitical risks and negative effects of inflation. If you want to get started with investing in metals such as gold and silver, read our free guide to gold buying in Canada in 2026 today.

In addition, if you find the prospect of life or business insurance complicated and overwhelming, there are resources to make life easier. For starters, BC residents can consult our guide of the Top 10 Life Insurance Providers in British Columbia (2026) for policy information on term, whole, universal, and no-medical life insurance, as well as detailed breakdowns and comparisons of each provider.

Similarly, homeowners and renters obtain the best deals when they shop around, and our guide on the Best 8 Ontario Home and Tenant Insurance Providers arms you with the best information to make an informed decision.

Third, if your company is located in Alberta or you’re running a small business with big ambitions, it’s essential to protect your assets and intellectual property from lawsuits, theft, personal injury, cyber attacks, or property damage that could derail your growth initiatives. Both guides outline excellent resources for obtaining business insurance in Alberta and across Canada.

Finally, for a comprehensive approach that only takes a few clicks, Zensurance is an online comparison site that works with more than 50 insurance providers to obtain the best coverage at the best price.

For additional resources, please consult our list of reliable lenders to see a wide range of products and services available in your area.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.