Prepaid cards like the KOHO Mastercard (www.koho.ca) have gone from niche product to mainstream money tool in Canada. A study by the Canadian Prepaid Providers Organization found Canadians increasingly reach for prepaid because they see it as more secure for online purchases and international travel than either credit or debit. KOHO has ridden that wave harder than anyone: more than 2 million Canadians now use it, and the company is deep into Phase II of its application for a Schedule 1 Canadian bank licence. So is the card actually worth a spot in your wallet in 2026? Here’s my full review.

Reduce your credit card payments by up to 30–50%

CCC is a non-profit credit counselling agency. Talk to a trained counsellor for free to see if you qualify for a debt management program and explore other options for relief, so you can avoid bankruptcy. They’ll work with your creditors to lower your interest rates and stop late fees, then roll everything into one monthly payment — so you can be out of debt in as little as 36 months. They are not a loan company and do not lend money.

BBB Rating: A+Trustpilot 4.7/5 (6,900+ reviews)500,000+ Canadians helped$1B+ in debt eliminated

Talk to a Counsellor for Free →

Results vary by debt type, creditors, and budget. This page isn’t legal advice.

About the Company

KOHO Financial is a Canadian fintech founded in 2014 by Daniel Eberhard. It issues prepaid Mastercards paired with a spending and savings app, and has grown into one of the country’s largest challenger banking platforms.

| Website | www.koho.ca |

| Phone | 1-855-564-6999 |

| Headquarters | Toronto, Ontario |

| Founded | 2014 |

| Users | 2 million+ Canadians |

| Trustpilot | ~4.5/5 “Excellent” (2,200+ reviews) |

| App Store | ~4.8/5 |

| Deposit Protection | Eligible for CDIC coverage up to $100,000 |

| Regulatory Status | Phase II of Schedule 1 bank licence application |

Two lines in that table deserve emphasis. First, the Trustpilot score: KOHO’s public reputation used to be its weak spot, with a rating that once languished below 2 stars. It now sits around 4.5 with an “Excellent” badge across thousands of reviews — one of the more dramatic reputation turnarounds I’ve tracked in Canadian fintech. Second, the bank licence: KOHO raised C$190 million in late 2024 (C$40 million equity, C$150 million debt) led by PROPELR Growth with Rockefeller Capital participating, in large part to fund its push to become a chartered bank. A fintech volunteering for full OSFI supervision is telling you something about its ambitions and its confidence.

What Is a KOHO Card and How Does It Work?

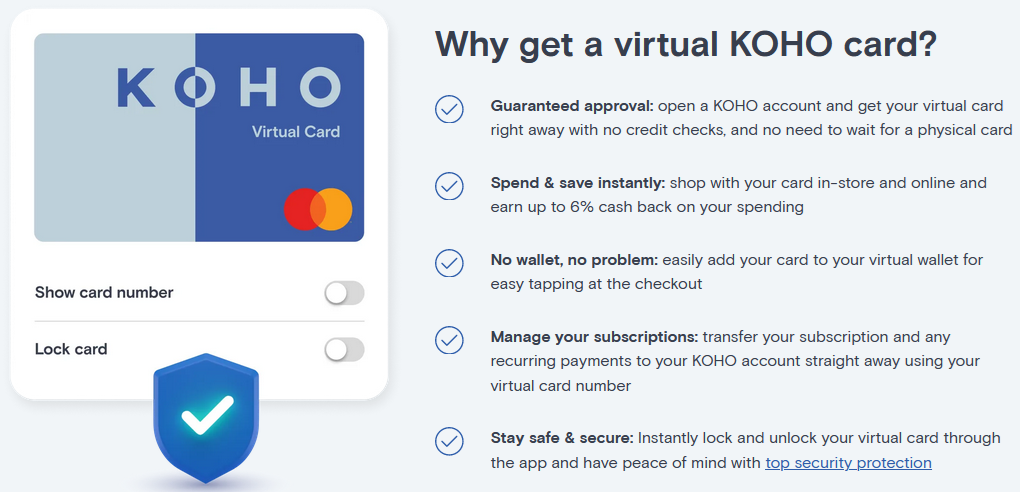

KOHO issues a prepaid Mastercard: you load money onto the card and spend it in-store or online anywhere Mastercard is accepted, earning cash back as you go and interest on whatever balance sits in the account. You get a virtual card instantly (loadable to Apple Pay or Google Pay) plus a physical card, and you can lock either one from the app in seconds.

One correction worth making plainly, because it’s a common misunderstanding: using the prepaid card by itself does not build your credit. Purchases on a prepaid card aren’t reported to Equifax or TransUnion — KOHO itself confirms this in its responses to reviewers. Credit building at KOHO happens through a separate paid subscription (and an optional secured line of credit), which reports your monthly payments to the bureau. It works, and it’s cheap, but it’s an add-on — I did a full breakdown of the costs and mechanics in my KOHO Credit Building review.

KOHO Plans and Pricing in 2026

KOHO no longer offers a free base plan to new customers, but the entry plan is easy to unlock at $0:

| Plan | Fee | Cash Back | Interest | FX Fees |

|---|---|---|---|---|

| Essential | $4/mo or $48/yr — free with recurring direct deposit or $1,000/mo in deposits | 1% on groceries, eating & drinking, transportation | 2% on your whole balance (opt-in) | 1.5% |

| Extra | $12/mo or $144/yr | 1.5% on those categories + 0.25% everywhere else | 2.5% | None |

| Everything | $22/mo or $177/yr (≈$14.75/mo billed annually) | 2% on those categories + 0.5% everywhere else | 3.5% | None |

All plans can earn boosted cash back — sometimes 5% or more — at KOHO’s partner merchants, and all come with a 30-day free trial. Extra and Everything add perks like one free international ATM withdrawal per month and a free monthly 1GB travel eSIM; the Everything annual plan includes a metal card.

A note from my spreadsheet: the interest rates are lower than they were at their promotional peak (long-time users will remember 4–5% offers), but 2–3.5% on an entire spending balance, calculated daily and paid monthly, still beats what the big banks pay on a chequing account by a wide margin — which is zero.

Other Features Worth Knowing

- CDIC eligibility. Funds are held with CDIC member institutions, making balances eligible for protection up to $100,000 — a big credibility upgrade over the prepaid cards of a decade ago.

- KOHO Cover. An optional interest-free cash advance of up to $250 for bridging to payday. If you’re comparing cash-advance apps, I’ve also reviewed Bree, which goes up to $750.

- Early payroll. Direct deposits are processed as soon as KOHO receives them, often the evening before payday.

- Round-ups, goals, and a free credit score in the app.

Find relief in 3 easy steps

1Talk to a counsellor for free

Review your debts, budget, and credit to see if you qualify — and explore other options so you can avoid bankruptcy.

2Start when you’re ready

Once you enrol, they call your creditors to lower your interest rates and stop late fees.

3Get out of debt faster

Make one monthly payment and they distribute it to your creditors — debt-free in as little as 36 months.

Tip: have your balances, minimum payments, and monthly expenses handy.

👍 KOHO Pros

- Guaranteed approval, no credit check. Applying takes minutes and won’t touch your credit file.

- Real yield on your balance. 2% to 3.5% interest on every dollar in the account, by plan.

- Meaningful cash back on the categories most budgets actually spend on, plus partner boosts.

- Easy $0 path. Direct deposit or $1,000/month in deposits makes the Essential plan free.

- CDIC-eligible deposits and instant card lock/unlock for security.

- A reputation on the upswing — Trustpilot has climbed from below 2 stars to roughly 4.5 “Excellent.”

👎 KOHO Cons

- The card alone won’t build credit. Bureau reporting requires the paid Credit Building add-on.

- Customer service remains the sore spot. The recurring complaint across platforms is slow chat support, and in some cases accounts frozen during identity re-verification with funds temporarily held. A lean digital-first operation buys you a great app and a thinner support bench — that trade-off hasn’t gone away.

- No free plan for new users. The $0 route exists, but it has conditions.

- Rates can change. Interest and cash-back rates have been adjusted before (mostly downward from promotional peaks) and can be again.

- Practical limits apply to ATM withdrawals and daily spending, and out-of-network ATM fees are on you.

How KOHO Compares

Against the big banks’ low-cost accounts, KOHO holds up very well. The Government of Canada’s low-cost account framework caps qualifying accounts at $4 per month — the same sticker price as KOHO Essential — but those bank accounts come with transaction maximums, no cash back, and no interest. A free-with-direct-deposit KOHO Essential simply delivers more per dollar, provided you’re comfortable banking from your phone.

Against fellow fintechs, the picture is more competitive. I’ve reviewed the Neo Money card, which fights KOHO hard on cash back partnerships, and Mogo, which bundles investing into its app. And whichever card you carry, keeping an independent eye on your file is smart — my Credit Verify review covers one of the monitoring options.

Final Thoughts: Are We Fans of KOHO?

Yes, with clear eyes about what it is. As a spending account, KOHO in 2026 is one of the best value propositions in Canada: free-able, cash back on real spending categories, genuine interest on the whole balance, CDIC-eligible, and backed by a company far enough along the bank-licence road that “fintech risk” concerns keep shrinking. The customer service complaints are real and worth weighing if you want a branch and a phone queue when things go wrong. And go in knowing the credit-building story accurately: the card is the spending tool; the credit repair happens through the paid add-on. For Canadians comfortable with app-first banking — and especially those rebuilding credit on a budget — KOHO remains an easy recommendation.

Bottom line: check your options now.

If you want one place to start, CCC is a strong option. You can get a clear recommendation based on your situation, and whether the best fit is a DMP or a principal-reduction route like a consumer proposal, they can help you move forward without bouncing between random companies.

FAQ

Is the KOHO card a real credit card?

No — it’s a prepaid Mastercard. You load your own money and spend it. That’s why approval is guaranteed and no credit check is needed.

Does using KOHO build my credit score?

Not by itself. Prepaid card purchases aren’t reported to the credit bureaus. KOHO’s separate Credit Building subscription (and optional secured line of credit) is what reports payments and moves your score.

How do I avoid the monthly fee?

Set up a recurring direct deposit (paycheque or government benefits) or deposit $1,000 or more into your account each month, and the Essential plan costs $0.

Is my money safe with KOHO?

Balances are held with CDIC member institutions and are eligible for deposit protection up to $100,000. KOHO is also progressing through Phase II of a Schedule 1 bank licence application.

What interest do I earn?

2% on Essential, 2.5% on Extra, and 3.5% on Everything — annual rates on your entire balance, calculated daily and paid monthly (opt-in required on Essential).

Mohammed Saqib has a Masters Degree from Wilfrid Laurier University in Waterloo. He has a robust background in accounting and finance. Mohammed started his career three years ago working as an investment analyst at a sell-side firm. He has extensively covered publicly-listed companies using fundamental analysis as the cornerstone of his approach. Mohammed has been published on SeekingAlpha, InvesorPlace, Yahoo! Finance and others.