With thousands of options available, choosing the right credit card can seem like a daunting task. Cash back? Travel rewards? Annual fees? And that’s before you even read the fine print.

Moreover, with traditional and digital banks battling for your businesses, should you choose the predictability of the Big 5, or opt for an upstart like Neo Financial?

Well, with the online bank offering unsecured and secured credit cards, let’s dive into the details to determine if they belong in your wallet.

About the Company

![]()

- URL: https://www.neofinancial.com/

- Phone: 1-855-636-2265

- Email: support@neofinancial.com

- Company HQ: Calgary, AB.

- Google Play Reviews: 4.2/5 stars (7,775 reviews)

- Trustpilot Reviews: 1.6/5 stars (89 reviews)

- Apple Store Reviews: 4.8/5 stars (31,466 reviews)

- BBB Reviews: 1.3/5 stars (99 reviews)

Neo Financial Pros and Cons:

To quickly determine the merits of Neo Financial’s credit cards, please see our list below:

Pros:

- Unsecured and secured options available

- Free and premium options available

- Great cash-back rates

- Guaranteed approval with a secured credit card

- Applying for a secured card won’t impact your credit score

- Cancel anytime without penalty

- Paid plans include additional services like legal advice, insurance, and credit monitoring

Cons:

- Poor customer service reviews

- Cash back is typically limited to partner company purchases

What Is Neo Financial?

Neo Financial is a fintech firm that offers financial services to millions of Canadians. Shunning the brick-and-mortar model, Neo Financial offers mobile and online banking, including checking, savings, credit card accounts, and mortgages.

In addition, Neo Invest helps you build investment portfolios based on your values, timelines, and risk tolerance. With up to three times more asset classes, you can diversify your holdings across alternative investments to enhance risk-adjusted returns. You can also opt for active accounts, and access portfolio management services through Neo OneVest.

Is Online Banking Safe?

With younger individuals familiar with mobile and online banking, Statistics Canada reported in March 2024 that “most Internet users aged 25 to 34 (90%), 35 to 44 (89%), and 45 to 54 (88%) managed a chequing or savings account online.”

However, with 82% of Canadian Internet users banking online in 2022 (up from 80% in 2018), the “growth was largely driven by adults aged 65 years and older: the proportion of older adults using online banking increased from 62% in 2018 to 70% in 2022.”

As a result, more Canadians have become comfortable with fintechs like Neo Financial, and the study noted how “the most popular method of payment online was a credit card, with almost 9 in 10 (89%) online shoppers using one to pay for their purchases.”

Thus, with Canadians’ banking habits moving in Neo Financial’s desired direction, digital adoption benefits the industry as a whole. And with regulations and in-house cybersecurity measures used to protect your data and privacy, online financial services remain a trustworthy resource.

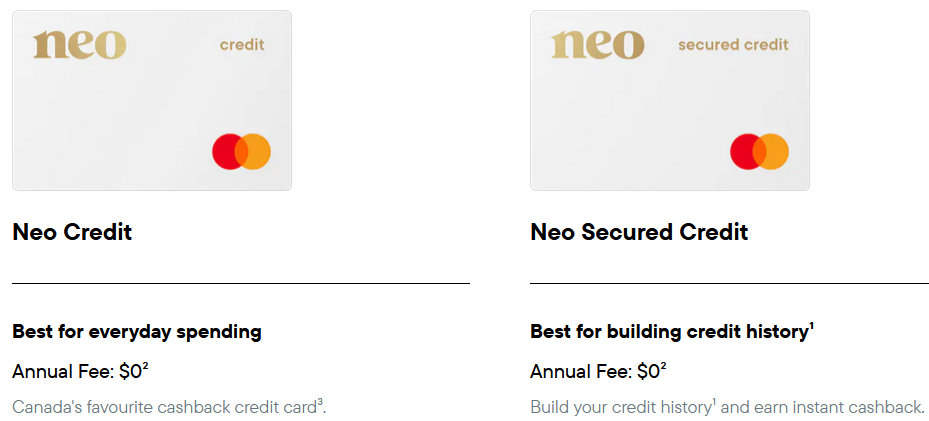

Why Choose a Neo Financial Unsecured Credit Card?

Whether you prefer fee or free, Neo Financial Canada has products that fit your needs. For example, two unsecured Neo Credit card options let you earn cashback at thousands of venues. The perks of the free plan include:

- Up to 5% cash back at restaurants and bars

- Up to 4% cash back at apps like Netflix, Disney+, Crave, Apple, Uber, Lyft, SkipTheDishes, DoorDash, UberEats

- 1% cash back on gas and groceries

However, if you choose a premium plan that costs $4.99 per month, the benefits include:

- Up to 6% cash back at restaurants and bars

- Up to 4% cash back at apps like Netflix, Disney+, Crave, Apple, Uber, Lyft, SkipTheDishes, DoorDash, UberEats

- 3% cash back on gas and groceries

- 0.5% cash back on all other purchases

As you can see, the premium plan includes more cash back for gas, groceries, and a higher maximum for restaurants and bars. On top of that, a premium Neo Credit card account includes:

- Credit Score Monitoring

- Purchase Protection

- 24/7 Legal Assistance

- $2,500 Group Life Insurance

- Personalized Insights

- Priority Customer Support

In addition, you can cancel your premium subscription at any time without penalty, and Neo Financial guarantees at least 0.5% cash back per month. So, if you choose the free plan and your partner purchases add up to less than 0.5%, Neo Financial will credit you the difference. But, please note the benefit maxes at $50 and only applies to purchases made at certain venues.

Finally, the purchase interest rate on a Neo Financial Credit card is 19.99%-29.99% and the cash advance rate is 22.99%-31.99%.

If you think you may need a cash advance, our Bree Loans review outlines why you should look elsewhere. In contrast to Neo’s 22.99%-31.99% cash advance rate, Bree offers free cash advances of up to $250, with no interest, fees, or credit check. The only catch is there is a $2.99 per month subscription fee, and you have to wait three days to receive the funds to avoid an express delivery charge. In addition, you may not receive a full $250 advance until the company knows you better.

What About a Neo Financial Secured Credit Card?

With the cost of living increasing since the pandemic, our Inflation Calculator CPI tables highlight how affordability remains challenging across the country. And with many Canadians confronting credit difficulties, a secured credit card can help rebuild your reputation if money woes have hurt your score.

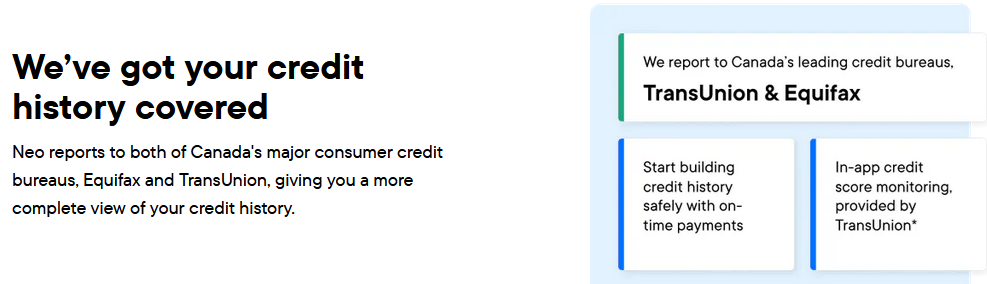

Highly rated among the personal finance community, a Neo Secured Credit card includes no hard or soft credit checks (won’t hurt your credit score) and guaranteed approval. You can set the deposit limit as low as $50, and borrowing against that amount helps rebuild your credit score when you make on-time repayments. Neo Financial Canada reports your payment history to TransUnion and Equifax.

Furthermore, the free and premium plans are identical to the unsecured options for the cost, interest rates, and cash-back rates. As such, you can choose a free or premium plan and enjoy the same terms and perks listed above.

KOHO vs. Neo: Which Has the Better Secured Credit Card?

In the battle of Canadian fintechs, KOHO and Neo Financial have similar secured credit cards that can improve your credit score. Our KOHO Credit Cards Review breaks down all the details, but the similarities include guaranteed approval and no credit check.

However, KOHO offers 1% cash back on most items, its prepaid credit card costs $4 per month, and KOHO waives the fee if you set up direct deposits or load $1,000 into your account each month. On the flip side, Neo offers more cash back and its premium plan costs $4.99 per month. So, while both products are worthwhile, the correct choice depends on your spending and deposit habits.

What Do Users Say About Neo Financial?

With solid metrics on the Apple App Store and Google Play, Neo Financial has ratings of 4.8 and 4.2 out of 5, with thousands of positive reviews. Conversely, Trustpilot and the Better Business Bureau (BBB) have ratings of 1.6 and 1.3. The positive reviews stated:

- Love this card!!!! accepted everywhere and easy to use. Rebates are amazing, and on almost everywhere I shop. As I was approved I was able to access the account from my Apple Pay. My card came in the mail quickly.

- Great app, works really well. Customer service is very impressive so far. I got both the credit card and savings and so far pretty happy with it. The cashback is the best I have seen on a credit card, lots of great deals, especially if you sign up for the paid version. Savings account got a great rate compared to any other bank.

On the other hand, the negative reviews stated:

- Only way to contact them is through chat. Makes you wait for thirty minutes and if you don’t respond immediately you need to restart and wait all over again. Can’t email them, can’t phone. Expect you to dedicate an hour of your day for simple problems thier automation hasn’t accounted for.

- I wanted to tell them that their ill-translated message in French looks like a spam message. That using Artificial intelligence is never a good idea. But can’t find a human to speak with.

Thus, Neo Financial Canada seems to have the same problems inherent with other fintechs. The products are great and they can offer better terms and rates due to their digital-only footprints. However, the lack of staff makes customer service problematic as technical issues can be time-consuming to remedy.

Consequently, Neo Financial is best suited for Canadians comfortable with online and mobile banking and who have the patience to troubleshoot issues via chat support.

How Do We Rate Neo Financial?

We believe Neo Financial is a solid option for Canadians who want a reliable credit card and value cash back. The perks are superior to similar options and partnering with Mastercard gives Neo Financial added credibility.

But, like most things in life, Neo Financial isn’t perfect, even if the customer service underperformance is common among fintechs. Therefore, Neo’s credit cards are great from a financial perspective, but whether they’re right for you depends on the services you value the most.

If you want to sign up or learn more, visit: www.neofinancial.com

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.