![]()

Looking for a way to cover a small shortfall before payday and build your credit at the same time? Nyble gives eligible Canadians an interest-free line of credit of up to $250 — with no credit check, no interest, and the bonus of reporting your on-time payments to the credit bureaus. With the cost of living still climbing in 2026, that combination of a fee-free buffer and credit building is hard to beat. Here’s our updated review — how it works, what it costs, who qualifies, and how it stacks up against alternatives like Bree.

⚡ Nyble at a Glance

- What it is: Interest-free, credit-building line of credit (not a payday loan)

- How much: $30–$250 (new users start lower and build up)

- Interest / APR: 0% — you repay exactly what you borrow

- Credit check: None, and no hard pull — applying won’t hurt your credit score

- Credit building: Reports on-time payments to Equifax & TransUnion

- Cost: Free base tier; optional $11.99/mo membership for extras & instant funding

- Funding speed: 0–3 business days free; ~30 minutes for members

- Rating: 4.8/5 on Trustpilot (9,000+ reviews) and 4.8/5 on the App Store

Compare 3 Canadian Interest-Free Alternatives

If you are interested in Nyble, you might also be interested in applying for these other interest-free alternatives who can also help you get cash while rebuilding your credit.

Quick take: Need money in your account today? Go with Bree (most cash) or Nyble (cash and credit building). Only rebuilding credit and don’t need spendable cash? Kikoff is built for that — but it’s a paid subscription and isn’t available in every province.

Nyble Pros and Cons

Here’s the quick verdict before we dig into the details:

✔ Pros

|

✘ Cons

|

Nyble vs. the Alternatives

When you’re short before payday, the usual options are a payday loan, overdraft, or simply eating the NSF fee. Here’s how those compare to Nyble:

| Option | Typical Cost | Builds Credit? |

|---|---|---|

| Nyble | 0% interest; free base tier | Yes |

| Payday loan | Often 100%+ effective APR | No |

| Bank overdraft | ~$5/month + interest | No |

| NSF (bounced payment) fee | Up to ~$50 per occurrence | No |

Need More Than $250? Consider Bree

If your shortfall is bigger than Nyble’s $250 cap, Bree is another strong interest-free option. Bree offers cash advances of up to $750 with 0% interest and no credit check, and its optional membership is cheaper ($2.99/mo vs. Nyble’s $11.99/mo). The trade-off: Bree doesn’t build your credit. So Nyble wins for credit-building and lower stakes; Bree wins for borrowing power. Many Canadians use both. See our full Bree review, or browse all our loans & cash advance guides.

What Is Nyble Canada?

When your paycheque is days away and bills are piling up, the usual options — personal loans, payday loans, or a credit-card cash advance — tend to come with long waits or high costs. Nyble is built to be the friendlier alternative.

Nyble (launched in 2022 by Fincentify Inc., based in Toronto) is a fintech that helps Canadians access cash and build credit at the same time. It provides an interest-free line of credit that works like a cash advance, and every time you repay, it reports the activity to bureaus like Equifax and TransUnion. Over time, consistent repayment can lift your credit score — useful if you’re working toward a mortgage, car loan, or better rates down the road.

Does Nyble Offer Loans?

Technically, Nyble does not offer traditional loans. Instead, it provides a small interest-free line of credit, usually between $30 and $250:

- ✅ No interest charges

- ✅ No credit check

- ✅ No traditional loan application

- ❌ Not a lump-sum loan like a bank or lender would offer

In other words, if you need a couple hundred dollars to bridge to payday, Nyble works like a short-term cash buffer — not a full personal loan like Alterfina, Spring Financial, or Journey Capital can provide.

How Nyble Builds Your Credit

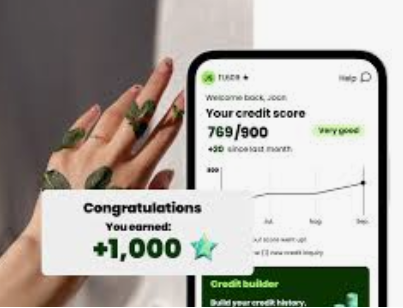

This is Nyble’s standout feature. Because it reports your payments to the credit bureaus, responsible use can actively improve your score. Nyble reports that eligible members who made on-time payments saw their Equifax Risk Score 2.0 rise by an average of ~36 points over three months (results vary, and late payments can lower your score).

Repaying on time and keeping balances low are the two biggest levers on a credit score, so a tool like Nyble pairs well with free monitoring such as Borrowell’s free credit report to track your progress. For more on the fundamentals, see our guide to how your credit score works.

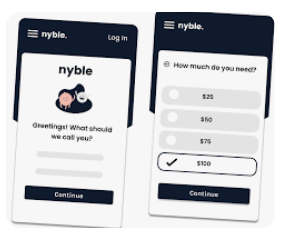

How Does Nyble Work?

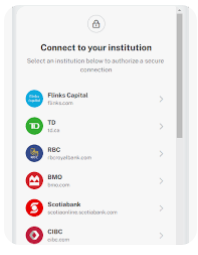

To qualify for a Nyble line of credit, you generally need:

- A Canadian bank account to verify your identity

- Recurring income — employment, government benefits (EI, pension), or a history of regular deposits

Once approved, you can draw an interest-free line of credit from $30 to $250. On your repayment date, Nyble debits the amount owing from your linked account and reports the repayment to the bureaus. If a payment is missed, Nyble reschedules the charge for the following day; missed payments are reported and can hurt your score — though, like a credit card, a missed payment generally won’t damage your credit if it’s resolved within 30 days.

Free members receive funds in zero to three business days, while members on the optional $11.99/month plan get funded in about 30 minutes and unlock extras like credit monitoring and identity-theft protection. If you can wait a few days, the free tier is all you need.

What Does Nyble Actually Cost?

The core service is interest-free and the base tier is free to use. Here’s the full picture:

| Interest / APR | 0% — always |

| Base line of credit | Free; funds in 0–3 business days |

| Membership (optional) | $11.99/month for instant funding, credit monitoring & ID-theft protection; cancel anytime |

| Tip | Voluntary; never required |

| Interest on what you borrow | None |

Instead of charging interest, Nyble relies on optional tips and the optional membership. The biggest real “cost” to weigh is the membership against how much value you get — if you only borrow occasionally, the free tier is the smarter choice.

Is Nyble Safe?

Nyble states that it protects your data with strong 4096-bit encryption and is PCI-compliant — and that it doesn’t sell your information to third parties. As a Canadian-built platform, it positions data privacy as a core feature, which matters given rising identity-theft concerns. As always, review the provider’s privacy policy before linking your bank account.

Are Customers Happy With Nyble?

Yes — Nyble holds a 4.8/5 rating on both Trustpilot and the App Store, across thousands of reviews. The themes are consistent:

- Positive: Reviewers highlight fast, easy approval, quick funding, and a no-judgment experience regardless of income or credit history — plus appreciation for the credit-building angle.

- Critical: The most common note is that early limits are small, and it takes consistent on-time repayments to work up toward the full $250.

Are We Fans of Nyble?

With 0% interest, a free base tier, and credit-building built in, Nyble is one of the best short-term options in Canada — especially if your goal is to rebuild credit while covering the occasional small gap. Free members can also track their credit score with weekly updates, so there’s very little downside to trying it.

The main limitation is the $250 cap, which makes Nyble a credit-builder rather than an emergency fund. If you need to borrow more, an interest-free option like Bree (up to $750) or a regulated lender such as Spring Financial may suit better. But for a fee-free buffer that also strengthens your credit, Nyble is hard to beat.

🎯 Cover a Gap and Build Credit

Access an interest-free line of credit up to $250 — no credit check, 0% interest, and on-time payments help build your score.

Carrying heavy, long-term debt rather than a short cash gap? Adding more credit won’t fix that. Learn about your options in our guides to debt consolidation in Canada and non-profit debt relief, or see if you qualify for help through Consolidated Credit Canada (free to check, won’t affect your credit score).

FAQ About Nyble

Is Nyble a legit company?

Yes. Nyble (operated by Fincentify Inc., based in Toronto) is a Canadian fintech offering interest-free, credit-building lines of credit. It’s rated 4.8/5 on both Trustpilot and the App Store across thousands of reviews. See Nyble here.

How much can I borrow from Nyble?

An interest-free line of credit from $30 to $250. New users typically start with a smaller amount and unlock more as they make on-time repayments.

Does Nyble charge interest?

No. Nyble charges 0% interest on what you borrow. The base tier is free; an optional $11.99/month membership adds instant funding, credit monitoring, and identity-theft protection.

Does Nyble do a credit check — and does it build credit?

There’s no hard credit check to apply, so signing up won’t lower your score. And because Nyble reports your payments to Equifax and TransUnion, on-time repayments can help build your credit over time.

Does Nyble do payday loans?

No. Nyble offers an interest-free line of credit, not a payday loan — there’s no required interest or fee, unlike high-cost payday lenders that can carry triple-digit APRs.

Is Nyble similar to Bree?

Both are interest-free with no credit check. Bree lends more (up to $750 vs. Nyble’s $250) with a cheaper membership, while Nyble’s edge is credit-building — it reports your payments to the bureaus. Choose based on whether you need more cash or stronger credit.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.