Windmill Microlending (www.windmillmicrolending.org) provides affordable career loans, coaching, and mentorship to help skilled newcomers restart or advance their careers in Canada. But is Windmill Microlending legit, and is one of its loans actually worth considering?

In this review, I’ll break down how Windmill works, who can apply, what the loan terms look like, how it compares to interest-free alternatives like Bree and Nyble, and when taking on another loan may not be the smartest move.

Quick Take: Is Windmill Microlending Worth It?

For eligible skilled immigrants and refugees in Canada, Windmill Microlending can be a useful option. The loans are designed for career-related expenses like licensing, exams, training, relocation, childcare, living expenses, and professional development.

Important: Windmill loans are not interest-free. Windmill currently lists its standard loan at a fixed 5.95% interest rate, with zero loan processing fees. That is still low compared with many credit cards, payday loans, and high-cost personal loans, but it is not the same as a 0% interest product.

Debt warning: If you are already struggling with credit card debt, missed payments, payday loans, collection calls, or more debt than you can realistically repay, taking on another loan may make things worse. Before borrowing more, consider comparing Canadian debt relief options.

About Windmill Microlending

![]()

- Website: https://www.windmillmicrolending.org/

- Phone: 1-855-423-2262

- Email: info@teamwindmill.org

- Who it serves: Eligible skilled immigrants and refugees across Canada

- Borrower feedback: ★★★★★ Strong online borrower ratings reported across review platforms

Windmill Microlending is a Canadian nonprofit organization that offers affordable loans and career support to immigrants and refugees. Its goal is to help skilled newcomers overcome financial barriers so they can re-enter their trained profession, upgrade their credentials, or move into work that better matches their education and experience.

The Government of Canada has also highlighted Windmill Microlending as an immigrant-serving organization that helps skilled immigrants and refugees access microloans for Canadian licensing, training, and career success. You can read more on Canada.ca.

From my perspective, this is what makes Windmill different from a regular lender. A bank may look mainly at your credit score, income, and risk profile. Windmill is looking at whether a newcomer has a realistic career plan and needs financing to get back into their field in Canada.

Windmill Microlending Pros and Cons

👍 Pros

- You can borrow up to $15,000 if eligible.

- Windmill lists a fixed low-interest rate as low as 5.95%.

- There are zero loan processing fees.

- Loans can be used for career-related expenses.

- Borrowers can access coaching, mentorship, and financial planning tools.

- The program is designed for skilled newcomers with limited Canadian credit history.

👎 Cons

- Windmill loans are not interest-free.

- You must meet newcomer and career-related eligibility rules.

- The application requires several documents.

- It is not a general-purpose emergency loan.

- A credit check may be required.

- Another loan can increase your debt burden if you are already stretched thin.

Are Windmill Microlending Loans Interest-Free?

No. Windmill Microlending loans are not interest-free. They are low-interest career loans for eligible skilled newcomers.

This matters because some Canadian fintech products, such as Bree and Nyble, are positioned as interest-free. However, those products are very different from Windmill.

| Product | Interest-Free? | Best For |

|---|---|---|

| Windmill Microlending | No. Low fixed interest applies. | Eligible skilled newcomers who need larger career loans for licensing, training, exams, relocation, childcare, or professional development. |

| Bree | Yes, generally positioned as 0% APR / no interest. | Small short-term cash advances for Canadians who need a smaller amount before payday. |

| Nyble | Yes, positioned as 0% interest. | Small credit-building needs and credit monitoring tools. |

So the simple comparison is this: Windmill may be more useful for larger, career-related newcomer expenses, while Bree and Nyble may be more relevant if you are looking for smaller interest-free cash flow or credit-building alternatives.

Who Can Apply for a Windmill Microlending Loan?

Windmill is mainly designed for skilled immigrants and refugees who want to restart or advance their careers in Canada.

Common eligibility requirements may include:

- Being an immigrant or refugee in Canada with eligible status, such as a Permanent Resident, Protected Person, Convention Refugee, Provincial Nominee, or Canadian Citizen.

- Having international education, professional training, or work experience before moving to Canada.

- Using the loan for a career-related purpose, such as licensing, accreditation, education, training, relocation, childcare, living expenses, or professional development.

- Not having an undischarged bankruptcy or a recent active consumer proposal that makes borrowing unsuitable.

If you are unsure whether you qualify, Windmill provides an eligibility check on its website. For other Canadian borrowing options, you may also want to read our guide on what to do if you need a loan but keep getting declined.

What Documents Do I Need When Applying?

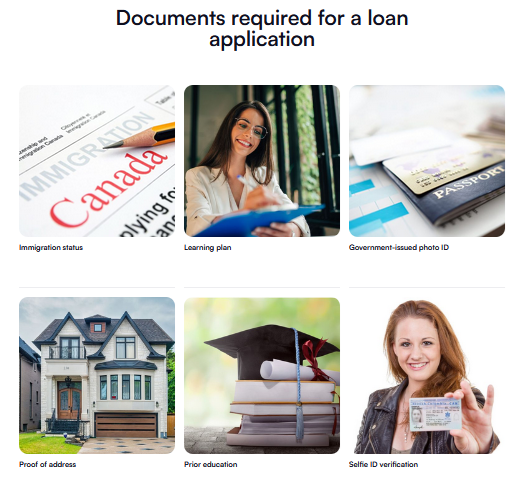

Before submitting an application, it is worth gathering your documents in advance. You may need:

- Government-issued photo ID

- Proof of address

- Documents verifying your immigration status

- Training or education documents verifying your credentials

- Evidence of education acceptance, if applicable

- Banking information

- A resume, which may help support your career plan

What Are the Loan Terms?

If you meet the eligibility criteria, Windmill Microlending currently advertises loans of up to $15,000, a fixed low-interest rate as low as 5.95%, zero loan processing fees, and free career coaching and mentorship. You can verify the latest details directly on Windmill’s official loan page.

| Maximum loan amount | Up to $15,000 |

| Interest rate | Fixed low-interest rate as low as 5.95% |

| Processing fees | Zero loan processing fees |

| Best used for | Licensing, exams, training, relocation, childcare, living expenses, and career development |

Please note that Windmill may review your credit history as part of the application. If a hard credit check is required, it could have a temporary impact on your credit score. If you are trying to rebuild your credit, you may also find our guide on how to improve your Canadian credit score helpful.

When Windmill Microlending Makes Sense

Windmill Microlending can make sense when the loan supports a clear path to higher income, better credentials, or professional advancement in Canada.

For example, an internationally trained nurse, engineer, pharmacist, accountant, IT professional, or tradesperson may need to pay for exams, bridging programs, professional memberships, relocation, childcare, or short-term living costs before returning to their career path.

In that situation, a low-interest career loan may be a productive form of borrowing because it is tied to a practical income-building goal.

When You Should Be Careful About Borrowing More

A loan can be helpful when it solves a specific problem, but it can also make things worse if you are already under a heavy debt burden.

You may want to avoid taking on another loan if:

- You are already missing payments on credit cards or loans.

- You are borrowing to pay for basic bills every month.

- You are using payday loans, cash advances, or overdraft to survive.

- You do not have a clear plan to repay the loan.

- You are being contacted by collection agencies.

If your main issue is overwhelming debt, the better first step may be to compare debt relief options instead of applying for a new loan. You can start with our guides on debt consolidation vs. consumer proposal in Canada, bankruptcy alternatives in Canada, and credit card debt in Canada.

Already Carrying Too Much Debt?

If your debt is already hard to manage, another loan may not be the safest solution. Before borrowing more, compare credit counselling, debt consolidation, debt management plans, consumer proposals, and other Canadian debt relief options.

How Do Borrowers Rate Windmill Microlending?

Windmill Microlending appears to have a strong borrower reputation, with many reviews praising its coaching, loan support, newcomer focus, and customer service. I would still check current ratings directly before applying, since review counts and scores can change.

Common positive themes include helpful career guidance, newcomer-friendly service, practical financing, and support that goes beyond the loan itself.

Do We Recommend Windmill Microlending?

Yes, for the right borrower. If you are an eligible skilled immigrant or refugee trying to restart your career in Canada, Windmill Microlending looks like a worthwhile resource to consider.

The biggest strengths are the low-cost structure, newcomer-specific eligibility model, career coaching, mentorship, and practical focus on professional advancement. I also like that the loan can be used for expenses that traditional lenders may not always understand, such as credential recognition, licensing exams, and bridging programs.

That said, it is still a loan, and it is not interest-free. You should apply only if the repayment fits your budget and the money supports a realistic career plan. Borrowing for education or career advancement can be worthwhile, but only when the expected return makes sense.

If you only need a smaller interest-free option, you may want to compare Bree or Nyble instead. Bree may be more relevant for small short-term cash advances, while Nyble may be more relevant for small credit-building needs. Neither is a direct replacement for Windmill, but they are worth understanding if your main goal is avoiding interest.

For example, our Borrowell Credit Report Review explains how free tools are available to help Canadians monitor and understand their credit. Responsible repayment of a Windmill loan may help build credit history if payments are reported and managed properly, while missed payments can hurt your credit.

If you want to sign up or learn more, visit: https://www.windmillmicrolending.org/

Need Debt Relief Instead of Another Loan?

If your debt is already becoming difficult to manage, the safest move may be to compare debt relief options before applying for more credit. A lower-interest loan can still become a problem if your total debt burden is already too high.

FAQ About Windmill Microlending

What is Windmill Microlending?

Windmill Microlending is a Canadian charity that provides affordable career loans, coaching, and mentorship to eligible skilled immigrants and refugees who want to restart or advance their careers in Canada.

Are Windmill Microlending loans interest-free?

No. Windmill loans are not interest-free. Windmill currently lists its standard loan at a fixed 5.95% interest rate, with zero loan processing fees.

How does Windmill compare to Bree or Nyble?

Windmill offers larger low-interest career loans for eligible skilled newcomers. Bree and Nyble are smaller interest-free options, but they are not direct replacements for Windmill because they serve different borrowing needs.

How much can you borrow from Windmill Microlending?

Windmill currently advertises loans of up to $15,000 for eligible borrowers. The exact amount you qualify for depends on your application, career plan, and repayment ability.

Should I take a Windmill loan if I already have high debt?

Be careful. If you already have high debt, missed payments, collection calls, payday loans, or credit card balances you cannot manage, another loan may make your debt burden worse. Compare debt relief options before borrowing more.

Is Windmill Microlending legit?

Yes, Windmill Microlending appears to be a legitimate Canadian charity focused on helping skilled immigrants and refugees rebuild their careers in Canada.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.