Blue Cross Life (CNW Group/Blue Cross Life)

Most Canadians know Blue Cross for health, dental and travel coverage — but the Blue Cross family also sells life insurance through Blue Cross Life Insurance Company of Canada. Its individual offering is straightforward: term life insurance, sold directly online, issued and underwritten by Blue Cross Life itself. In this review we’ll cover how it works, what it offers, what drives the cost, the drawbacks worth knowing about, and how it stacks up against two popular online alternatives we’ve reviewed — PolicyMe and North Cover.

One thing to understand up front: the broader Blue Cross family includes several independent regional plans best known for health and dental benefits. The life insurance covered in this review is different — it’s offered by Blue Cross Life Insurance Company of Canada, a federally licensed insurer operating across the country, and it’s bought directly through Blue Cross Life’s own online platform rather than through a regional benefits plan. Unlike many digital-first insurers that sell policies backed by a third-party underwriter, Blue Cross Life is both the issuer and the underwriter of its policies.

How Blue Cross Compares to Competitors

Blue Cross is one of three online-friendly options we rate highly, but they suit different people. Here’s our quick verdict on where each one wins. (We’ve left universal-life-via-MGA distributors like IDC out of this table on purpose — those are sold through advisors, not bought directly, so they’re not an apples-to-apples comparison.)

Quick take: All three can be bought online, but they’re built differently. PolicyMe is our best-overall pick for healthy term buyers. Blue Cross stands out if you want your policy issued and underwritten directly by an established Canadian insurer — no third-party underwriter in the middle — with level premiums and a fully digital purchase. North Cover is a useful no-underwriting bridge, just go in knowing its premiums increase every year.

Blue Cross Life Insurance: Pros and Cons

✔ Pros

|

✘ Cons

|

What Blue Cross Life Insurance Offers

Blue Cross Life keeps its individual offering deliberately simple: one product, term life insurance, designed to deliver practical, reliable financial protection without unnecessary complexity.

Term life insurance

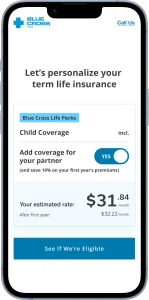

Term lengths run from 10 to 30 years, so you can align coverage with real-life financial responsibilities — paying off a mortgage, raising children, or covering other large expenses until they wind down. Coverage amounts range from $100,000 up to $5 million, and premiums stay level for the term you choose, so budgeting is predictable from day one. The entire purchase happens online through Blue Cross Life’s e-commerce platform, and the policy is issued and underwritten by Blue Cross Life itself. This is the product most families should price first — it’s the cleanest comparison against our best term life providers roundup.

If your goal is permanent coverage or a more complex estate-planning structure, that’s outside what Blue Cross Life sells directly online — it’s worth speaking with a licensed advisor and reading up on estate planning before committing to those longer-commitment products.

How Much Does Blue Cross Life Insurance Cost?

Your premium depends on factors like age, sex, smoking status, health, coverage amount and term length. Two structural points work in your favour on cost: premiums are level for the entire term — a meaningful contrast with rising-premium products like North Cover’s flagship policy — and the fully online, direct model keeps the process fast and simple. Because rates are personal, the only number that matters is your own: quotes are free and take a few minutes online.

Who Should (and Shouldn’t) Choose Blue Cross

Blue Cross is a strong fit if you: want term life coverage issued and underwritten directly by an established Canadian insurer rather than a third-party-backed policy; like the reassurance of a nationally recognized brand; want a fully online purchase with no advisor appointments; and want level premiums you can budget around for 10–30 years.

Look elsewhere if you: want permanent coverage like whole or universal life (Blue Cross Life’s direct online product is term only); need a small policy under $100,000, such as final-expense coverage; or prefer to buy through a human advisor. It’s always smart to price at least two providers — start with our best term life providers in Canada roundup and our PolicyMe review.

Reputation & Backing

The Blue Cross name is one of the most recognized insurance brands in the country, with decades of experience serving millions of Canadians. For life insurance specifically, the structural point that matters most is that Blue Cross Life is both the issuer and the underwriter of its policies — your coverage is backed directly by a federally licensed Canadian insurer, not routed through a third-party provider. That combination of a traditional insurer’s credibility with a modern, fully digital purchase experience is the core of the pitch, and in our view it holds up.

How to Apply & Make a Claim

Applying is straightforward and happens entirely online: get a quote on Blue Cross Life’s platform, complete the application questions about your health and lifestyle, and once approved, your policy takes effect after you review it and make the first payment. For a claim, the beneficiary contacts Blue Cross Life, submits the claim forms plus the death certificate, and the tax-free benefit is paid to the named beneficiaries once approved.

Our Verdict on Blue Cross Life Insurance

Blue Cross Life earns a solid recommendation. Its formula — level-premium term life, $100,000 to $5 million in coverage, flexible 10–30 year terms, bought entirely online from an insurer that issues and underwrites its own policies — is exactly what most Canadian families shopping for straightforward protection need. In our overall ranking of the providers we review individually, we’d place it second — behind PolicyMe as our best-overall pick, but ahead of North Cover, largely because Blue Cross keeps premiums level while North Cover’s flagship structure raises them every year. As with any insurer, pull your own quote — pricing is personal, and comparing two or three providers takes minutes.

Blue Cross Alternatives Worth Comparing

Before you settle, it’s smart to compare at least two or three options — rates and underwriting differ a lot between insurers:

- PolicyMe — our top pick for healthy Canadians who want fast, affordable term life underwritten by Securian Canada.

- North Cover — a no-underwriting option backed by Teachers Life; useful as a bridge, but note its premiums rise annually.

- Best term life providers in Canada and best no-medical companies — our wider roundups for a full shortlist.

Blue Cross Life Insurance FAQ

Is Blue Cross a single life insurance company in Canada?

The Blue Cross family includes several independent regional plans best known for health, dental and travel coverage. Individual term life insurance, however, is offered by Blue Cross Life Insurance Company of Canada — a federally licensed insurer that issues and underwrites its own policies and sells them directly online across the country.

What life insurance products does Blue Cross Life sell online?

One product: term life insurance. Term lengths run from 10 to 30 years, with coverage amounts from $100,000 up to $5 million. Permanent products like whole or universal life aren’t part of the direct online offering.

Is Blue Cross life insurance available in my province?

Blue Cross Life is federally licensed and operates across Canada, and its term life insurance is sold through a direct-to-consumer, fully online platform — so you don’t need to go through a regional benefits plan to buy it.

Do Blue Cross term premiums increase over time?

No — Blue Cross Life term premiums stay level for the term you choose. That’s a key difference from some no-medical products (such as North Cover’s flagship policy) where premiums are adjusted upward each year.

How does Blue Cross compare to PolicyMe?

Both offer fully online term life in Canada with level premiums and coverage up to $5 million. The structural difference: PolicyMe policies are underwritten by Securian Canada, while Blue Cross Life issues and underwrites its own policies. Since pricing is personal, the smart move is to pull a quote from both — each takes only a few minutes.

Planning your family’s finances more broadly? Life insurance is one piece. It’s also worth reading up on estate planning, keeping an eye on how inflation in 2026 affects how much coverage you actually need, and — if debt is part of the picture — our guides to debt relief options.

Disclosure: we’re an independent blog and may earn a commission from some of the providers mentioned, at no extra cost to you. This doesn’t influence our rankings, which are based on product features, pricing, backing and customer reputation. This article is for general information only and isn’t financial or insurance advice — we don’t provide insurance recommendations or suitability assessments for your personal situation. Confirm current rates and product details with the insurer before buying.

Mark Turner is a retired financial writer that now enjoys blogging about different financial topics, such as commodities, inflation, debt, retirement, alternative investments and Canadian politics.