Keeping an eye on your credit score is one of the smartest, cheapest financial habits you can build. Credit Verify (creditverify.ca) is one of the paid subscription services that offers to do it for you. But before you hand over a card number, there’s a lot you need to know — because this is a service I’d approach with real caution, and I’ll explain exactly why. In this review I’ll cover what Credit Verify offers, what its billing model actually looks like, what its reputation says in 2026, and the free alternatives that do most of the same job.

Reduce your credit card payments by up to 30–50%

CCC is a non-profit credit counselling agency. Talk to a trained counsellor for free to see if you qualify for a debt management program and explore other options for relief, so you can avoid bankruptcy. They’ll work with your creditors to lower your interest rates and stop late fees, then roll everything into one monthly payment — so you can be out of debt in as little as 36 months. They are not a loan company and do not lend money.

BBB Rating: A+Trustpilot 4.7/5 (6,900+ reviews)500,000+ Canadians helped$1B+ in debt eliminated

Talk to a Counsellor for Free →

Results vary by debt type, creditors, and budget. This page isn’t legal advice.

Quick Overview

Credit Verify is a subscription-based credit monitoring service based in Squamish, British Columbia. It offers credit score tracking, credit report access, identity-theft alerts, and financial-education resources — the standard feature set for this category.

| Official Name | Credit Verify |

| Website | creditverify.ca |

| Phone | 1-866-899-3175 |

| Location | Squamish, British Columbia |

| Model | Paid subscription (typically a $1 trial converting to a recurring monthly charge) |

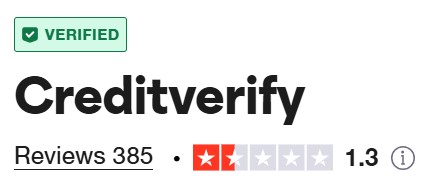

| Trustpilot | ~1.3/5 across 400+ reviews |

That Trustpilot score is not a typo, and it’s the single most important number in this review. A 1.3 out of 5 across hundreds of reviews isn’t a run of bad luck — it’s a pattern. Coming from a background where I spent my days reading financial disclosures, I’ve learned that when the complaints all rhyme, you should listen to the melody.

The Billing Model Is the Whole Story

Here’s what the reviews describe again and again: users sign up expecting a free or $1 credit check — often to “verify identity” — and then discover a recurring charge (commonly around $35/month) hitting their card a week or a month later. Many say the recurring subscription wasn’t clear at signup, and that cancelling was difficult, with some reporting repeated charges even after they thought they’d cancelled.

Credit Verify’s response, which it posts publicly to these reviews, is that the $1 trial and the ongoing subscription cost are disclosed during signup through a series of tick-box confirmations and a welcome email, with a 7-day window to cancel without charge. So the company’s position is that the terms are there to be read. The problem, from a consumer standpoint, is that a service generating this volume of “I didn’t realize I was subscribing” complaints has a disclosure design that isn’t working for a lot of the people using it — whatever the fine print technically says.

A second, more serious pattern shows up in recent reviews: people report being funnelled to Credit Verify by a fake job offer. A supposed recruiter asks the applicant to “verify” themselves by signing up and sending a screenshot. That’s a well-known scam structure, and while it’s the scammers running it rather than the company itself, it’s a red flag worth naming plainly. If anyone ever tells you to sign up for a credit-check service as a condition of a job, stop — that is not how legitimate hiring works.

Independent scam-checking sites also flag creditverify.ca with a low trust score. None of this makes using the service impossible, but it raises the bar for why you’d choose a low-rated paid option over the free ones below.

Find relief in 3 easy steps

1Talk to a counsellor for free

Review your debts, budget, and credit to see if you qualify — and explore other options so you can avoid bankruptcy.

2Start when you’re ready

Once you enrol, they call your creditors to lower your interest rates and stop late fees.

3Get out of debt faster

Make one monthly payment and they distribute it to your creditors — debt-free in as little as 36 months.

Tip: have your balances, minimum payments, and monthly expenses handy.

What Credit Verify Offers

To be fair, the underlying service does exist and does function. The feature set includes:

- Credit score monitoring with alerts when your score moves.

- Credit report access so you can review your history.

- Identity-theft alerts flagging suspicious activity on your file.

- Financial education resources in a member library.

- Customer support by phone, email, and live chat.

The issue isn’t that these features are fake. It’s that every one of them is available elsewhere for free, without a recurring charge that reviewers struggle to cancel.

👍 Pros

- Real, functioning features. Score monitoring, report access, and identity alerts all work as described.

- One consolidated dashboard for people who prefer everything in one interface.

- Multiple support channels — phone, email, and chat.

👎 Cons

- A ~1.3/5 Trustpilot rating across 400+ reviews — among the worst in the category.

- Billing complaints dominate. Surprise recurring charges after a $1 “trial” is the recurring theme.

- Cancellation friction. Numerous reviewers describe difficulty stopping the subscription and getting refunds.

- You’re paying for free things. Everything here is available at no cost from the bureaus and free apps.

- Scam-adjacent marketing. Third parties use fake job offers to funnel sign-ups, and independent sites flag the domain.

The Free Alternatives You Should Try First

This is the part I’d underline. Under Canadian law, you have the right to your credit report from both national bureaus for free, and the government says so directly. The Financial Consumer Agency of Canada’s guide to getting your credit report and score explains every method — and it includes an explicit warning that fraudsters pose as free-credit-report providers to harvest your personal and financial information. Read that page before you pay anyone.

Concretely, here’s the free stack I’d use instead:

- Equifax and TransUnion directly. Both are legally required to give you a free credit report — online, by phone, by mail, or in person. A smart habit is to alternate: pull one bureau every six months so you’re checking your file twice a year at zero cost.

- Free score apps. Borrowell (Equifax data) and Credit Karma (TransUnion data) both show your score and report highlights for free, funded by product offers rather than subscription fees. I went deep on one of them in my Borrowell review.

- Your own bank app. Many Canadian banks and credit unions now display a free credit score right inside their mobile app.

If your real goal is understanding or fixing your score rather than just watching it, my guide to improving your Canadian credit score is more useful than any monitoring subscription, and my breakdown of R-ratings like R2 explains what the codes on your report actually mean. If debt is the underlying worry, a free consultation with a non-profit like Consolidated Credit Canada will do more for you than a paid alert every time your balance changes.

Is Credit Verify Right for You?

For the overwhelming majority of people, my answer is no — not because the features don’t work, but because you can get the same monitoring free and skip the billing headaches that define this company’s review history. The only scenario where a paid all-in-one service makes sense is if you specifically want bundled identity-theft monitoring in a single dashboard and you’re comfortable managing the subscription carefully. Even then, I’d compare it against better-rated paid options before landing on one sitting at 1.3 stars.

If you do sign up for any $1-trial service, set a calendar reminder to cancel before the trial ends, screenshot your cancellation confirmation, and watch your statement for the following two billing cycles.

Bottom line: check your options now.

If you want one place to start, CCC is a strong option. You can get a clear recommendation based on your situation, and whether the best fit is a DMP or a principal-reduction route like a consumer proposal, they can help you move forward without bouncing between random companies.

FAQ

Is Credit Verify a scam?

The service itself is a real, functioning credit-monitoring product, so calling it a “scam” outright isn’t quite accurate. However, it holds a ~1.3/5 Trustpilot rating driven by complaints about surprise recurring charges after a $1 trial and difficulty cancelling, and third parties have used fake job offers to funnel sign-ups. Approach with caution.

Is Credit Verify free?

No. It typically starts with a $1 trial that converts into a recurring monthly subscription (commonly around $35). The company says these terms are disclosed at signup; many reviewers say they didn’t realize they were subscribing.

How do I cancel Credit Verify?

You can cancel through the member portal, by phone at 1-866-899-3175, or by mail. Reviewers report the process can be difficult, so keep written confirmation and monitor your statements afterward.

How can I check my credit for free instead?

Request free reports directly from Equifax and TransUnion (online, phone, mail, or in person), use free apps like Borrowell or Credit Karma, or check your bank’s app. The FCAC outlines every free method.

Why does a job recruiter want me to use Credit Verify?

That’s a scam warning sign, not a legitimate hiring step. No real employer requires you to sign up for a paid credit-check service. Do not proceed.

Mohammed Saqib has a Masters Degree from Wilfrid Laurier University in Waterloo. He has a robust background in accounting and finance. Mohammed started his career three years ago working as an investment analyst at a sell-side firm. He has extensively covered publicly-listed companies using fundamental analysis as the cornerstone of his approach. Mohammed has been published on SeekingAlpha, InvesorPlace, Yahoo! Finance and others.