Want to rebuild your credit score and get access to a quick cash advance from the same app? That’s the pitch behind KOHO’s credit-building tools. The real question is whether it delivers. In this review I’ll walk through how KOHO’s credit building and Cover cash advance work, what they cost in 2026, and whether they’re worth it.

☝IMPORTANT 2026 TIPS:

➔ Exhausted by existing debts? Contact Consolidated Credit Canada to see if you qualify for up to 50% off debt relief.

➔ Rejected for financing by a traditional lender? For loans through alternative lenders, check Swoop. (Expect higher interest rates!)

About the Company

KOHO is a Canadian fintech, founded in 2014 by Daniel Eberhard, that offers cash-back spending accounts, a prepaid Mastercard, secured borrowing, and credit-building tools. It has grown into one of the country’s largest neobanks, with more than 2 million users and an $800 million valuation, and it’s currently working through a Schedule 1 bank licence application that would make it one of Canada’s first fintech-native banks.

- KOHO Cover (cash advance): koho.ca/cover

- KOHO Credit Building: koho.ca/creditbuilding

- Phone: 1-855-564-6999

- Email: support@koho.ca

- Headquarters: Vancouver, BC (601 West Broadway, Suite 400)

- Trustpilot: ~4.5/5 (“Excellent”), 2,100+ reviews

- App Store: Highly rated, ~4.8/5 (often the #1 Canadian finance app)

- BBB: Not accredited; active complaints on file (mostly account closures and disputes)

- Card partner: Mastercard. Backers include Drive Capital, Portag3, TTV Capital, HOOPP, Round13, and the BDC.

A note on the ratings: KOHO’s Trustpilot score has shifted substantially over time. As of 2026 the live Canadian Trustpilot page shows a TrustScore around 4.5 across more than 2,000 reviews, a far cry from the low ratings the company carried a couple of years ago. The BBB picture is more mixed, with ongoing complaints centred on account freezes and withheld funds, so it’s worth reading both sides before you commit.

KOHO Pros and Cons

👍 Pros

- Reasonably priced. Credit building is a small monthly add-on, not a big upfront cost.

- No interest on Cover cash advances. You pay a flat membership fee, not interest.

- Works for decent and bad credit. No hard credit check to start credit building.

- Reports to the credit bureaus. Repayment activity is reported, which is what actually moves your score.

- Builds credit over time. KOHO cites an average increase of 31+ points in about four months.

- No hidden fees. Pricing is laid out plainly across plans.

👎 Cons

- Credit building is a paid add-on. It runs $5 to $10 per month depending on your plan, on top of any plan fee.

- No more free plan. KOHO discontinued its free “Easy” plan in 2024; the cheapest plan now carries a small monthly fee (waivable on Essential).

- Not everyone qualifies for every product.

- Mixed service reviews. App ratings are strong, but customer-service complaints (especially around account closures) are a recurring theme.

2026 Pricing: How KOHO’s Numbers Actually Break Down

KOHO’s pricing has two separate pieces that often get muddled together. Keeping them straight matters, because they’re not the same thing.

1. Interest earned on your balance (money KOHO pays you)

- Everything plan: 3.5%

- Essential plan: 2%

2. The Credit Building add-on fee (what you pay for the feature)

- Essential or Easy plan: $10/month

- Extra plan: $7/month

- Everything plan: $5/month (Everything gets 50% off credit building)

3. The plan fees themselves

- Essential: about $4/month (free with direct deposit or $1,000/month loaded)

- Extra: about $9/month

- Everything: about $22/month

So the all-in cost of credit building depends on which plan you’re on. If you’re on Essential and just want the credit-builder, you’re effectively paying the $10 add-on (with the plan fee waived via direct deposit). On Everything, credit building is only $5 thanks to the 50% discount, but the plan itself costs more. There’s no single “credit building price”; it’s the combination that matters.

Who Is KOHO Financial?

KOHO is a full-service fintech offering cash-back spending accounts, a KOHO credit card, secured borrowing products, and its credit-builder program. The company’s whole pitch is no hidden fees and no fine print. Its card partner is Mastercard, and its backers include Drive Capital, Portag3, TTV Capital, HOOPP, Round13, and the BDC.

You can reach KOHO’s support team seven days a week through the app or website, or by calling 1-855-564-6999. One honest caveat from my years analyzing financial firms: a lean, digital-first operation (KOHO runs with roughly 250 employees serving millions of users) tends to deliver a slick app but slower human support. That trade-off shows up clearly in the reviews.

☝IMPORTANT 2026 TIPS:

➔ Exhausted by existing debts? Contact Consolidated Credit Canada to see if you qualify for up to 50% off debt relief.

➔ Rejected for financing by a traditional lender? For loans through alternative lenders, check Swoop. (Expect higher interest rates!)

How Important Is My Credit Score?

A single number doesn’t capture everything about your finances, but it carries real weight. As the Government of Canada notes, businesses use your credit report and score to gauge how risky it is to lend to you, and a higher score can earn you a lower interest rate, which saves money over the life of a loan.

For context, Canadian credit scores run from 300 to 900, broken down as:

- 300–579: Poor

- 580–659: Fair

- 660–719: Good

- 720–779: Very Good

- 780+: Excellent

KOHO credit building won’t rocket you from poor to excellent overnight, but it can nudge your score in the right direction. If debt is the bigger problem, you can also look at consolidating with Consolidated Credit Canada.

How Does KOHO Improve My Credit Score?

KOHO’s credit building gives you two routes:

- Credit Building — you open a line of credit with KOHO, and on-time “repayments” are reported to the bureaus.

- Flexible (Secured) Credit Building — you set aside your own funds ($30 to $500) as security for the line of credit, then borrow against that balance.

With the secured option, you deposit $30 to $500 to create the secured line, move a portion (KOHO suggests around 10% of the balance) into your spending account, and on your next billing date KOHO automatically moves it back. Those transfers count as debt repayments, and KOHO reports the activity to the credit bureaus that set your score. There’s only a soft credit check to enrol, so applying won’t ding you.

The secured route is the better fallback if your credit history is badly damaged, since an unsecured line might only approve a small amount. After signing up, your current score appears in-app, then updates as KOHO reports your payments. KOHO cites an average increase of 31+ points in about four months, and it also reports rent payments to Equifax, which helps the roughly 40% of Canadians who rent and otherwise get no credit benefit from it.

One reminder: repayment is tied to your billing date, not the day you moved money. If your billing date is September 5 and you moved funds on August 28, payment is due September 5.

What’s the Catch?

To use the secured credit-building option, you first subscribe to credit building, which (as covered above) costs $5 to $10 per month depending on your plan. The Flexible (secured) program carries a $5 monthly service fee plus the $30–$500 you set aside as security.

The bigger catch is symmetry: just as on-time payments help your score, a missed payment gets reported too and can hurt it. Credit building cuts both ways, so only enrol if you’re confident you can keep the payments current.

If KOHO isn’t the right fit, you can also look at alternative lenders like Swoop.

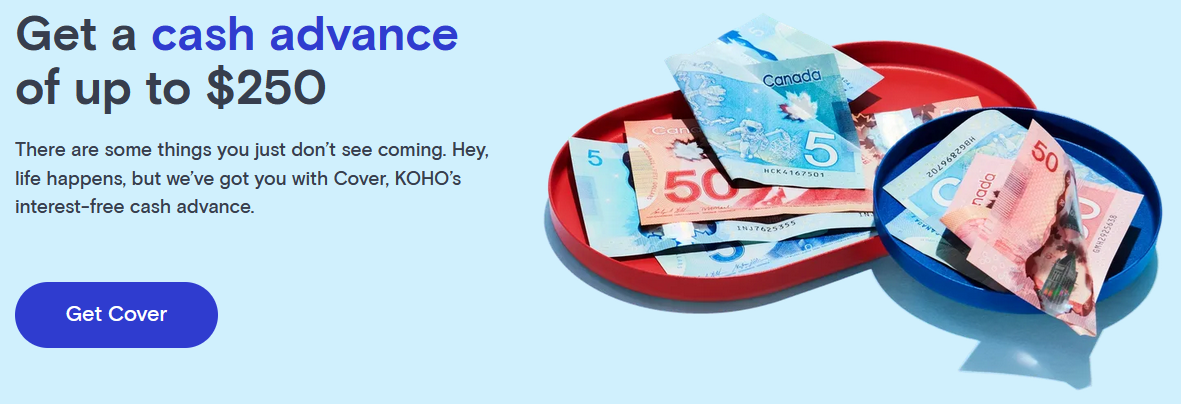

KOHO Cover Cash Advance

KOHO Cover is the cash-advance side of the app, and it’s a useful product for short gaps. It provides $2 to $250, with guaranteed approval, no credit check, and no interest. You pay a $2/month membership fee, and KOHO’s algorithm sets your limit based on your financial data. KOHO notes the fee can vary based on the advance amount and other factors, so different users may see slightly different terms.

You access the funds through the app or at an ATM, and you can raise your limit over time by using the app regularly, repaying on time, paying bills from your account, and enrolling in credit building.

What sets Cover apart from products like Bree is repayment flexibility: you can repay whenever you want, rather than having it automatically pulled from your next paycheque. Both products help you sidestep overdraft fees that can run $50 or more, but KOHO bundles it with a wider set of services.

How Do Users Rate KOHO?

KOHO’s reviews have improved markedly. The live Canadian Trustpilot page now shows an “Excellent” TrustScore around 4.5/5 across more than 2,000 reviews, with recent feedback praising the app, the interest on balance, the cash back, and the credit-building tools. The mobile app is consistently among the top-rated Canadian finance apps, with an App Store rating near 4.8.

That said, the picture isn’t uniformly glowing. The recurring complaint, on Trustpilot and especially the BBB, is customer service: slow chat support, and in a number of cases, account closures with funds held during identity re-verification. The pattern is familiar for a digital-first fintech, but it’s a real consideration if you’d want fast human help when something goes wrong.

So weigh what you value most. If you want a strong app and low-cost credit building, KOHO scores well. If hands-on, immediate support is a deal-breaker, factor that in. Alternative lenders like Swoop can also be worth a look.

☝IMPORTANT 2026 TIPS:

➔ Exhausted by existing debts? Contact Consolidated Credit Canada to see if you qualify for up to 50% off debt relief.

➔ Rejected for financing by a traditional lender? For loans through alternative lenders, check Swoop. (Expect higher interest rates!)

My Verdict on KOHO

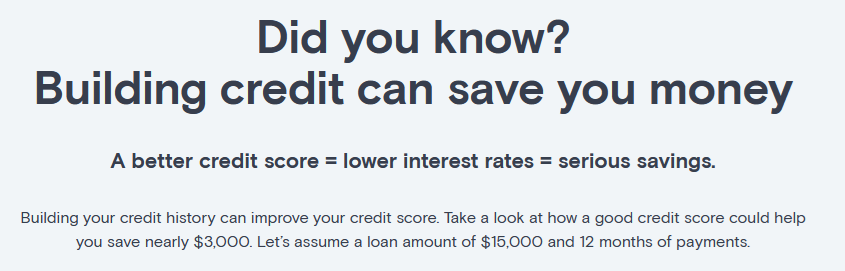

There’s a lot to like, but it isn’t perfect. Credit building costs $5 to $10 per month depending on your plan, and customer service can be hit-or-miss. The upside is that the program does work, and the savings from a better credit score can dwarf those monthly fees.

Here’s the math I’d point to. A $5,000 personal loan at 10% interest, repaid over two years, costs about $537 in interest. The same loan at 9% costs about $482, and at 8% about $427. Shaving two points off your rate saves roughly $110 — and that’s on a single small loan. On a car loan or mortgage, the gap compounds into real money. That’s the case for treating a few dollars a month in credit building as an investment rather than a cost.

So while KOHO’s credit-builder programs aren’t for everyone, I’d consider them worthwhile for Canadians with bad or very bad credit who can commit to on-time payments. If your bigger issue is existing debt, Consolidated Credit Canada is another avenue for relief.

Mohammed Saqib has a Masters Degree from Wilfrid Laurier University in Waterloo. He has a robust background in accounting and finance. Mohammed started his career three years ago working as an investment analyst at a sell-side firm. He has extensively covered publicly-listed companies using fundamental analysis as the cornerstone of his approach. Mohammed has been published on SeekingAlpha, InvesorPlace, Yahoo! Finance and others.