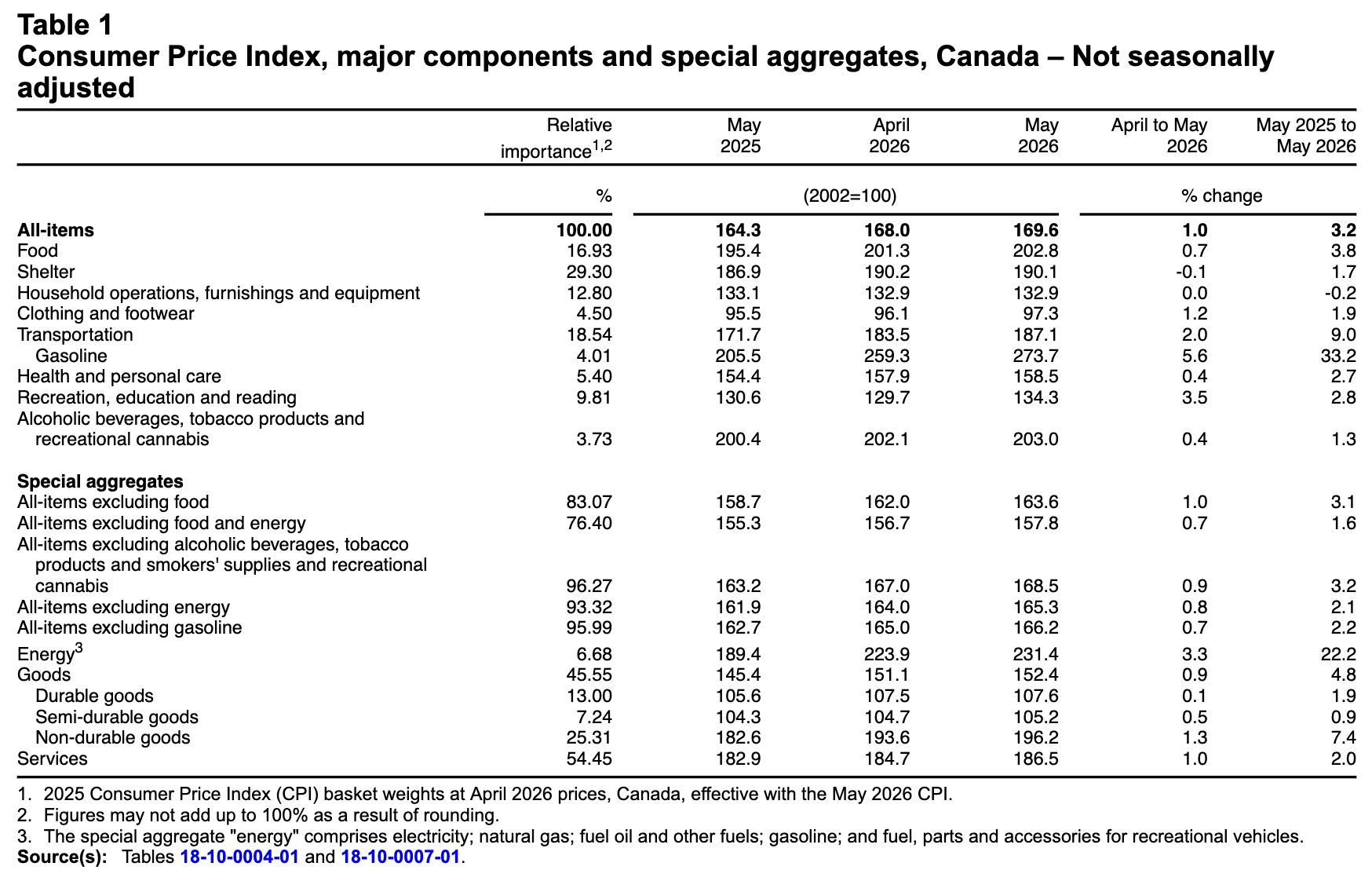

Canada’s consumer price index (CPI) increased by 3.2% year over year (Y-o-Y) in May, up from 2.8% Y-o-Y in April. Statistics Canada (StatsCan) published the data at 8:30 a.m. ET on June 22, 2026, via The Daily report. On a monthly basis, the CPI rose by 1.0%, as “Higher prices for gasoline continued to drive the acceleration in the headline CPI.”

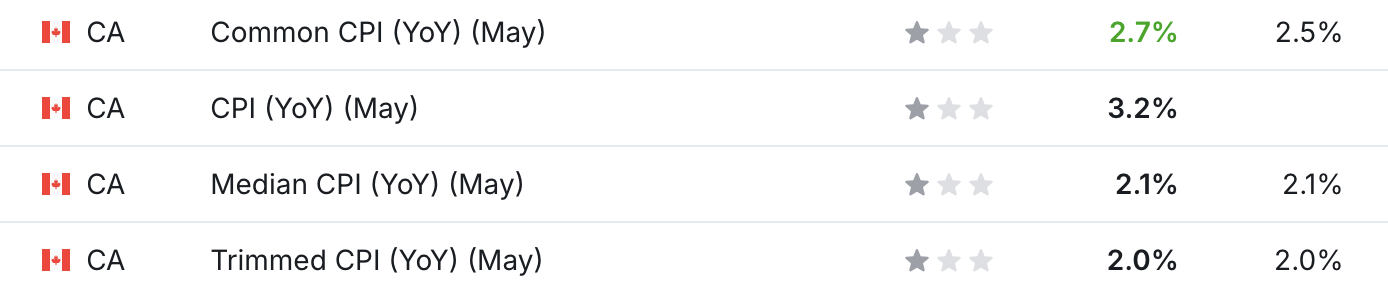

Despite that, the results mostly aligned with economists’ expectations. The table below is courtesy of Investing.com. The left column represents May’s figures, while the right column represents forecasters’ consensus estimates. As you can see, the common CPI was the only core measure in green.

Yet, the U.S.-Iran deal helps alleviate some of the near-term pressures. With oil prices declining significantly, the weakness should help suppress the headline CPI. And with the core CPI largely aligning with the Bank of Canada’s (BoC) target, the committee may be able to look past the recent shock. As a result, the labour market may become the main concern if trade restrictions arise in the back half of the year.

Core CPI

Core measures of the CPI were mostly mild in May, with the CPI-common index rising to +2.7% (from +2.5%), the CPI-median holding at +2.1% (from +2.1%), and the CPI-trim holding at +2.0% (from +2.0%). These measures exclude the impacts of food and energy, and the BoC places heavy emphasis on core measures because they provide a smoothed distribution of overall inflation.

Please note that food and energy prices are highly volatile and price spikes can occur for reasons outside of the BoC’s control. In contrast, core inflation is mainly driven by consumer demand and gives the BoC a better sense of how the Canadian economy is functioning.

Sector Results

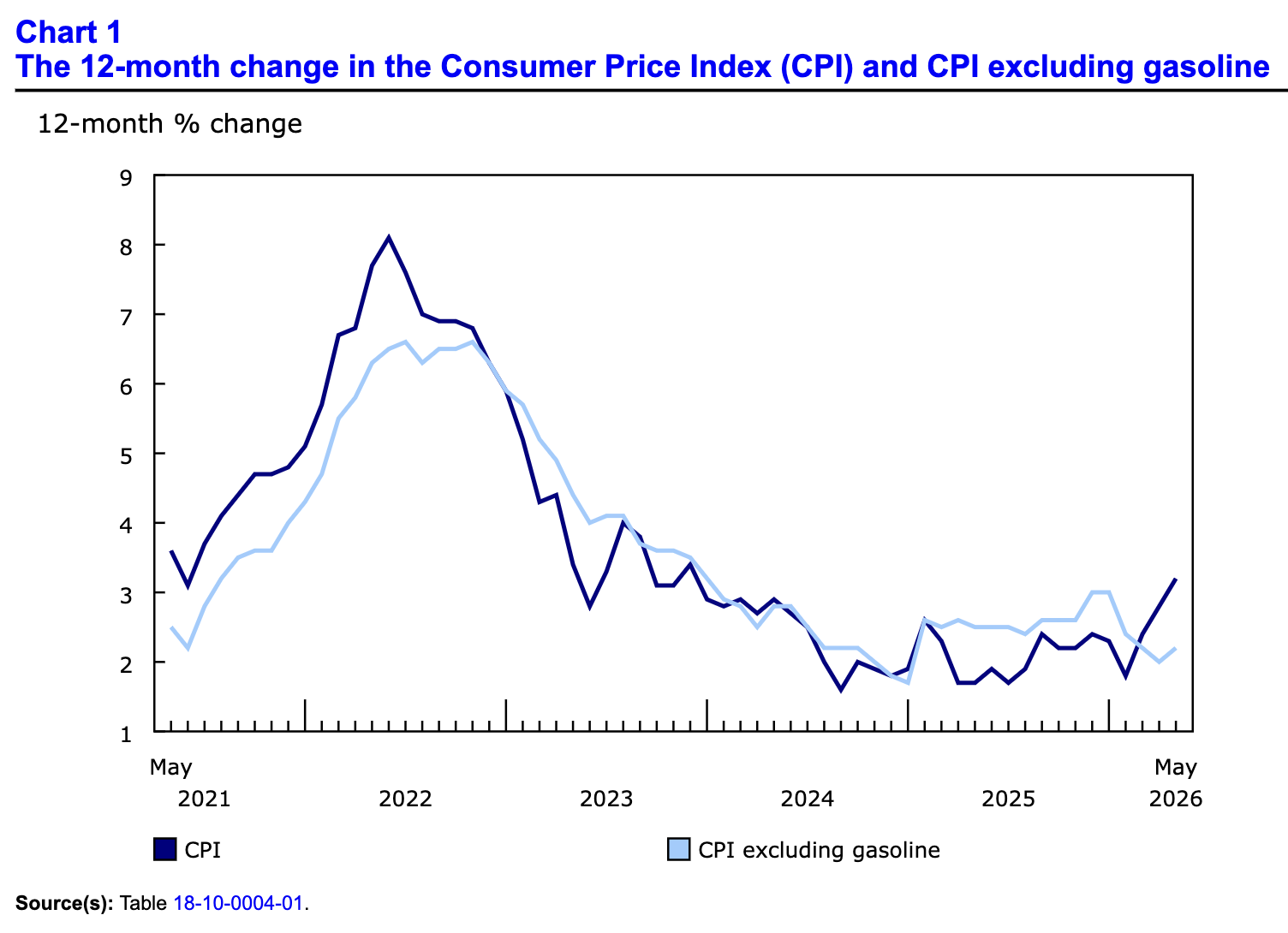

Sector performance was mixed in May, as transportation was a noticeable Y-o-Y outlier once again, while recreation and food also outperformed their April results.

For context, the eight sectors include food, shelter, household operations, furnishings and equipment, clothing and footwear, transportation, health and personal care items, recreation and education expenses, and alcohol and tobacco products.

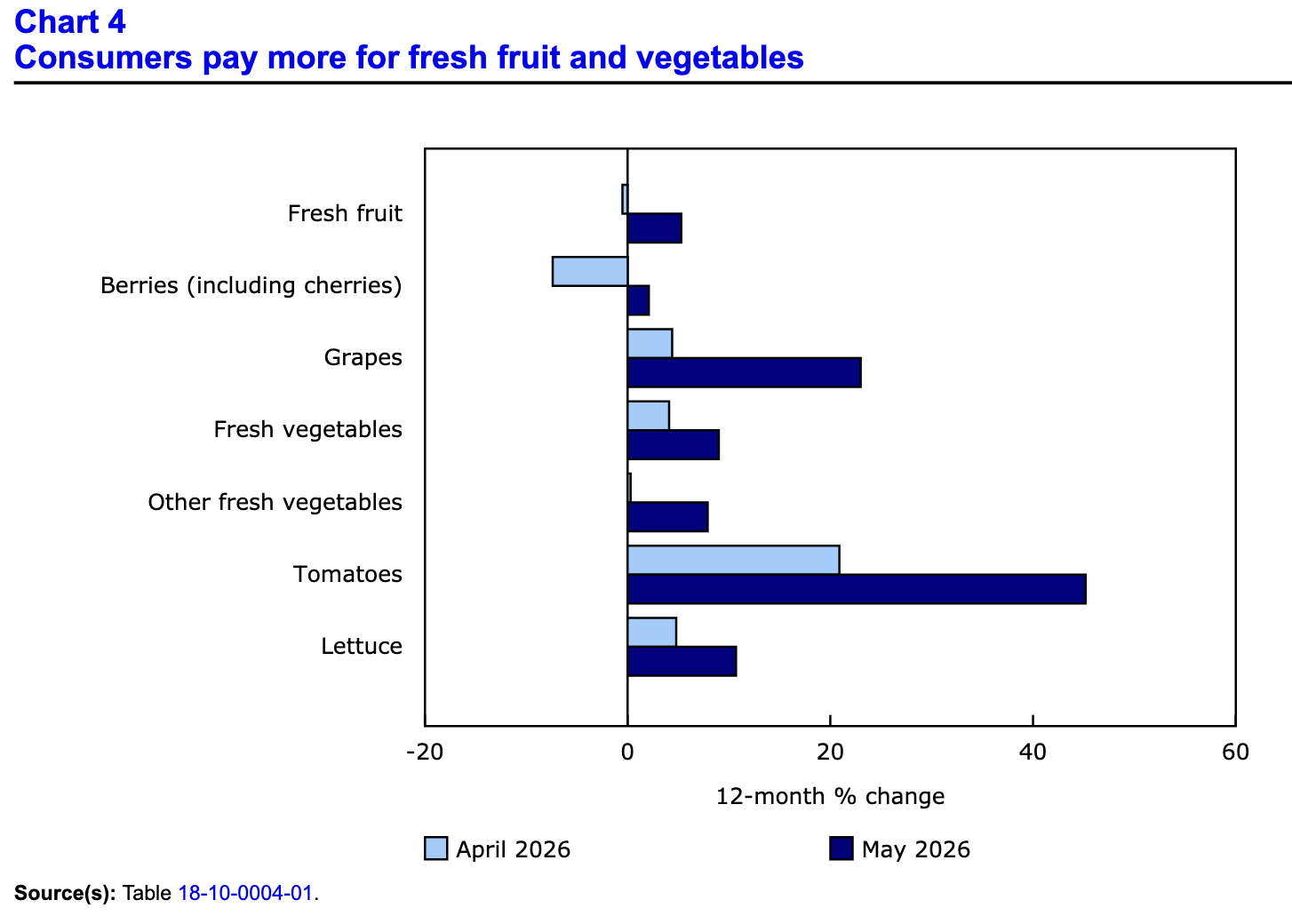

Food Inflation

Consolidated food prices rose by 0.7% on a monthly basis in May, driven by fruits and vegetables. The release noted how “Prices for fresh fruit rose at a faster pace year over year in May (+5.3%) compared with April (-0.5%). The acceleration was mostly driven by berries and grapes.”

In addition, “prices for fresh vegetables increased 9.0% in May, following a 4.1% rise in April. The upward movement was attributed to higher prices for broccoli, cauliflower, tomatoes, and lettuce. Tomato prices rose 45.2% in May due to supply contractions in Mexico.”

Add it all up, and food purchased from stores has increased Y-o-Y for 16 straight months.

Bad News

While inflation was the primary concern for investors and policymakers, Canada slipped into a technical recession after two consecutive quarters of negative real GDP growth. And with the CUSMA negotiations a potential catalyst for even more economic weakness, the outlook remains troublesome.

For example, the U.S. can officially opt out of the CUSMA deal by exercising a six-month termination clause. If so, it could be a repeat of 2025 and cause major chaos for an already weak Canadian economy. Market participants typically front-run these events, and with the CAD/USD in free fall recently, the Canadian dollar’s sharp decline highlights how institutions expect tough times ahead.

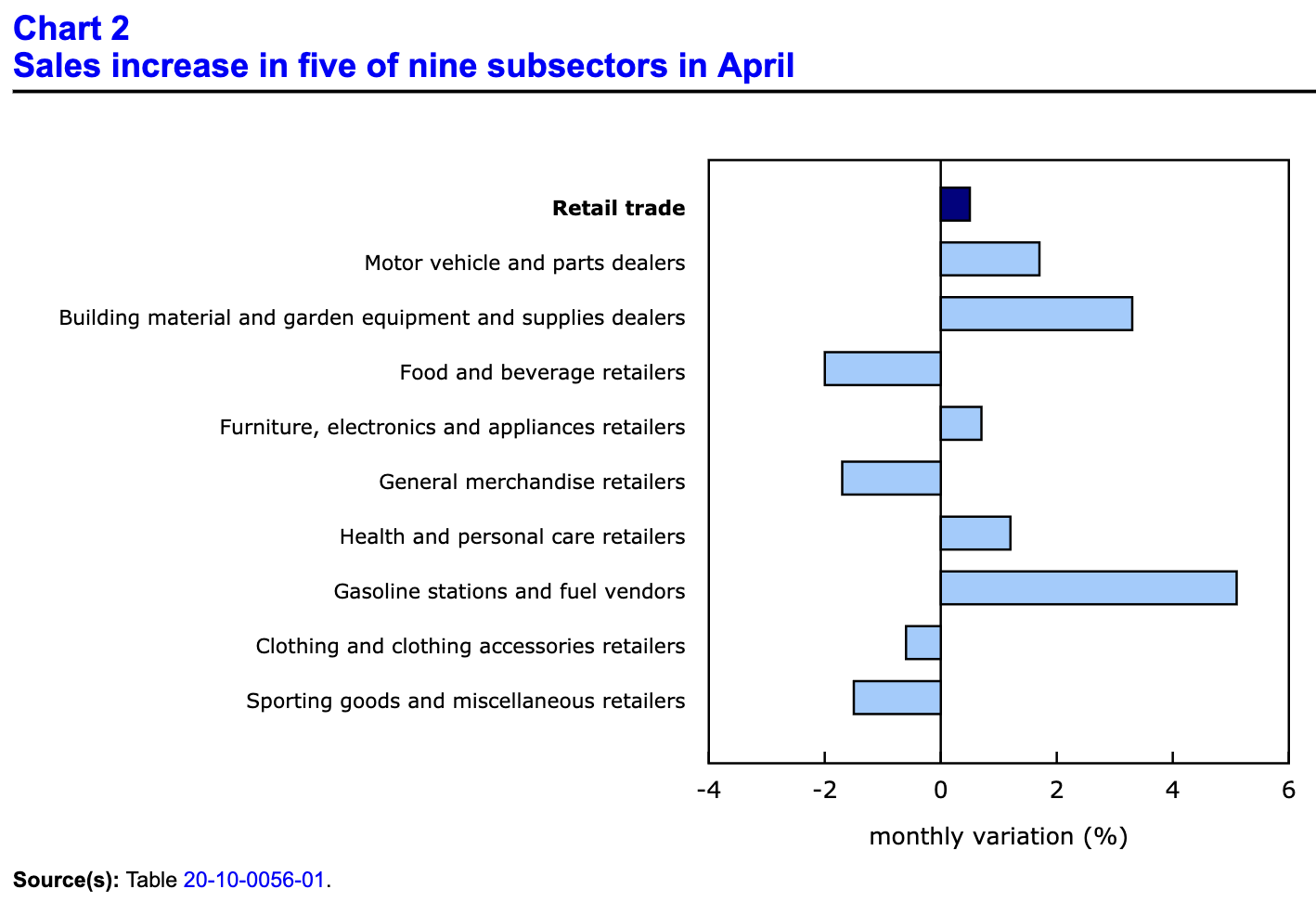

Furthermore, Statistics Canada revealed on Jun. 19 that “Core retail sales fell 0.7% in April, posting their second consecutive monthly decline. The decrease was led by lower sales at food and beverage retailers (-2.0%) and general merchandise retailers (-1.7%).”

Thus, while higher gasoline and fuel prices uplifted the headline figure, overall spending remains weak.

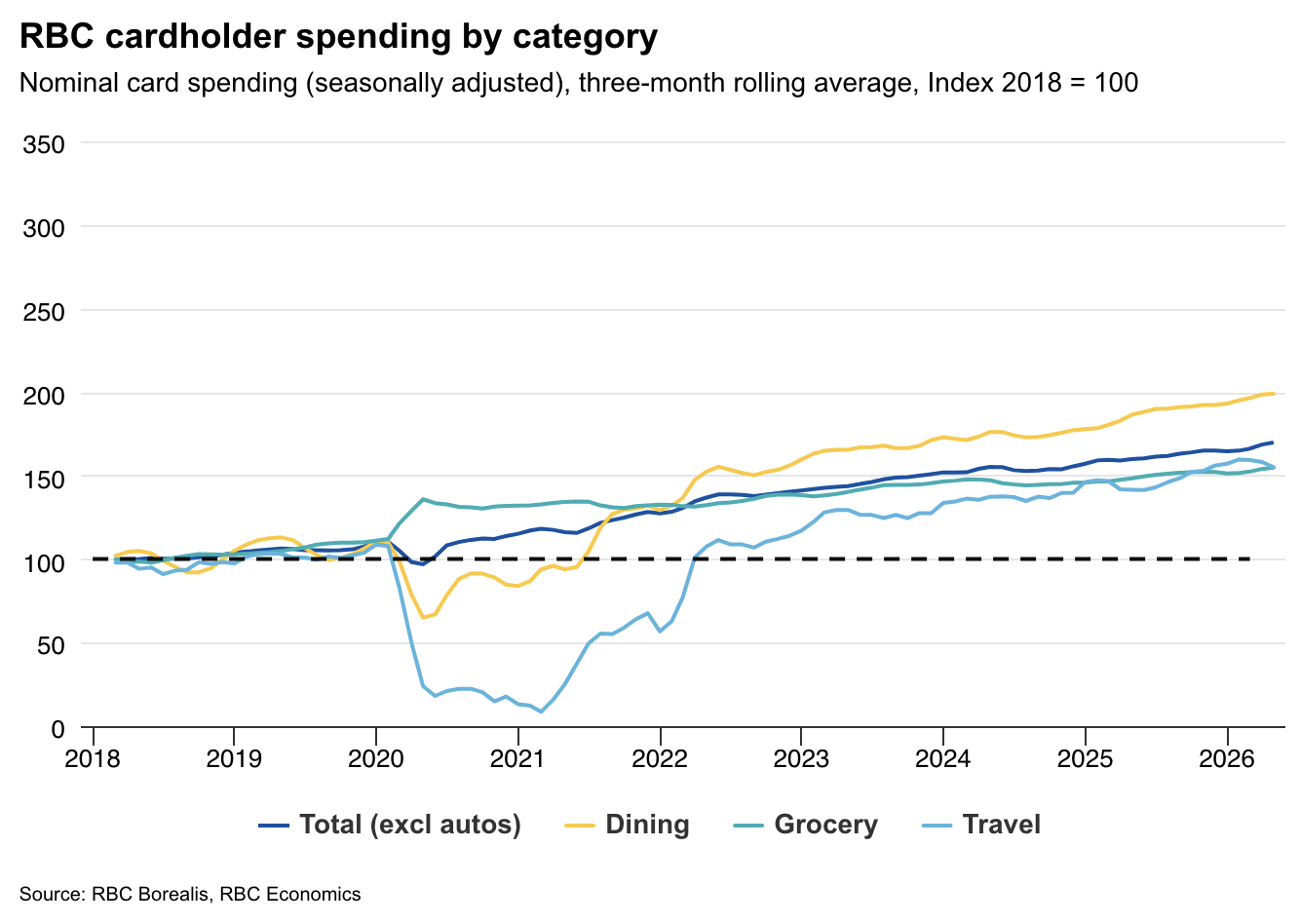

Similarly, while RBC’s Consumer Spending Tracker painted a mixed picture, the report noted how “Higher gasoline prices continued to absorb a larger share of household budgets. However, limited pullback in spending by consumers on other goods and services implies households continue, for now, to dip into savings (or increase borrowing) to keep spending.”

So, while the data were better than the Statistics Canada release, borrowing and/or using savings to spend is unlikely to generate sustainable economic growth. Therefore, the BoC may worry less about inflation in the second half of 2026, and instead, focus more on consumption, employment, and potential trade uncertainty.

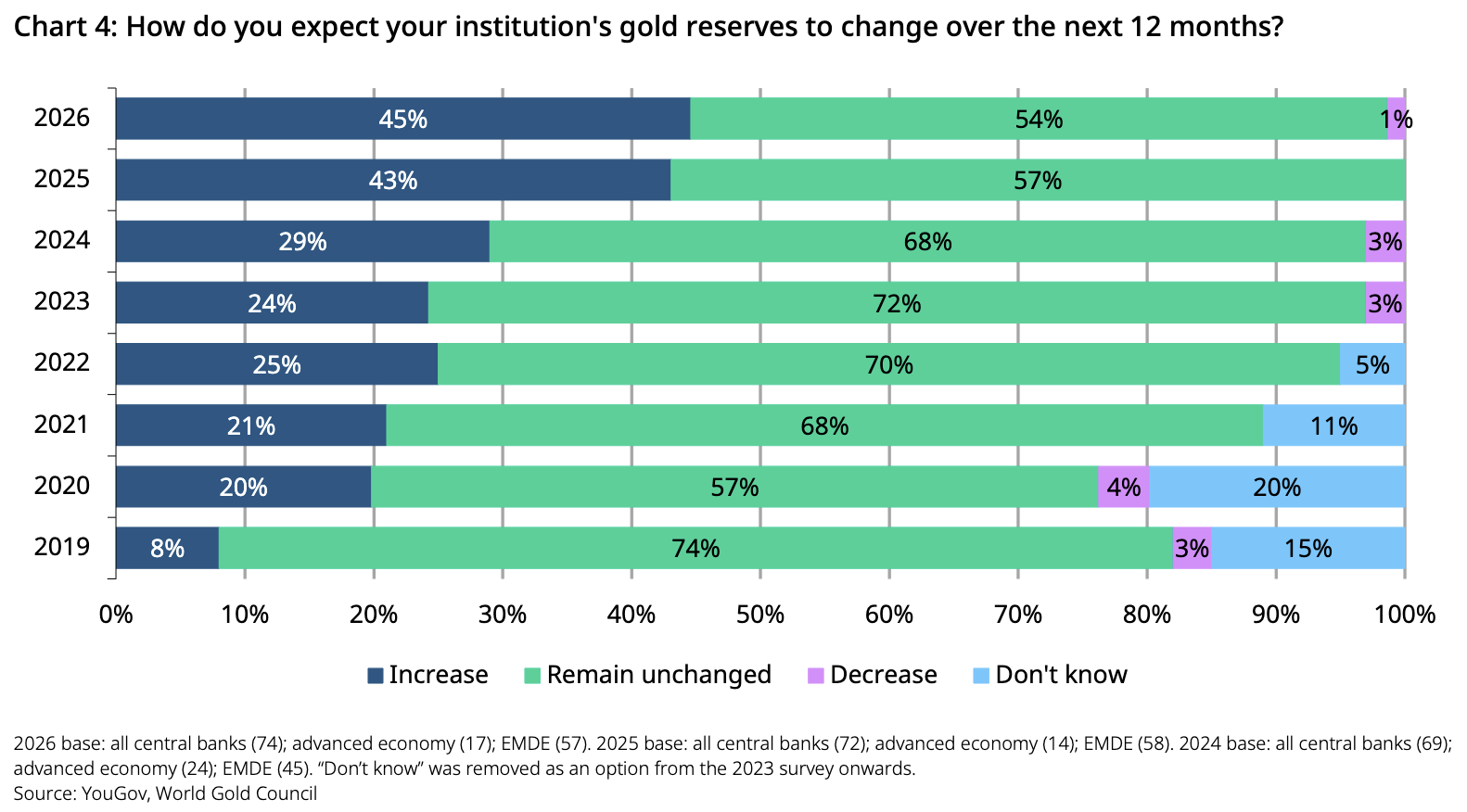

Turning to the financial markets, gold continues to struggle alongside the recent chaos, and higher global interest rates and a stronger U.S. dollar are a bad combination for the yellow metal. However, the long-term outlook remains constructive.

The World Gold Council noted in its latest June 2026 central bank survey that “a record 45% of respondents expect their own gold reserves will also increase over the same period. The majority of the remaining respondents indicated they expect no change, while 1% expect their institution’s gold reserves to decrease.”

As such, the largest institutions with unlimited buying power plan to keep stockpiling gold over the next 12 months.

Dedicating a small portion of one’s TFSA or RRSP portfolio to precious metals may help mitigate some of the geopolitical risks and negative effects of inflation. If you want to get started with investing in metals such as gold and silver, read our free guide to gold buying in Canada in 2026 today.

In addition, if higher interest rates have made borrowing unaffordable, several reputable companies can help you rebuild your credit and qualify for cheaper products.

Nyble and Bree are top performers, as the former provides Canadians with interest-free lines of credit that work like a cash advance. Every time you repay, the activity is reported to bureaus like Equifax and TransUnion, which helps boost your credit score. The latter (Bree) is similar, but it doesn’t report your payment activity to credit bureaus, so it’s more of a payday-loan alternative than a credit builder. Kikoff sits in the middle, as it’s a credit-building platform that doesn’t offer loans and isn’t available in all provinces. As a result, since there are pros and cons of each, you should read the full reviews to determine which product is right for you.

For aspiring drivers with less-than-stellar credit, we also know 15 subprime car loan providers that can get you back on the road. Or, if you’re in the market for life insurance, our extensive guide covers the best options available in Ontario.

For additional resources, please consult our list of reliable lenders to see a wide range of products and services available in your area.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.