If aggressive creditors, missed payments, or a tight paycheque caused you to search for payday loan alternatives in Canada, you are not alone. Payday loans are marketed as quick fixes for short-term cash problems, but they can be one of the most expensive ways to borrow money.

In my opinion, payday loans should usually be treated as a last resort, not a first choice. I have reviewed Canadian financial products and debt solutions for more than two decades, and the pattern is hard to miss: small emergency loans can turn into a much bigger debt problem when the fees, repayment timing, and repeat borrowing cycle are not handled carefully.

This guide looks at safer payday loan alternatives in Canada, including banks, credit unions, credit counselling, Bree, Nyble, KOHO, Borrowell, and debt relief options for people who are already carrying too much debt.

Already Carrying Too Much Debt?

If you are already behind on credit cards, using payday loans repeatedly, receiving collection calls, or struggling to make minimum payments, another loan may not solve the real problem. It may simply delay it.

Before borrowing more, compare debt consolidation, credit counselling, debt management plans, consumer proposals, and other Canadian debt relief options.

Why Payday Loans Are Risky

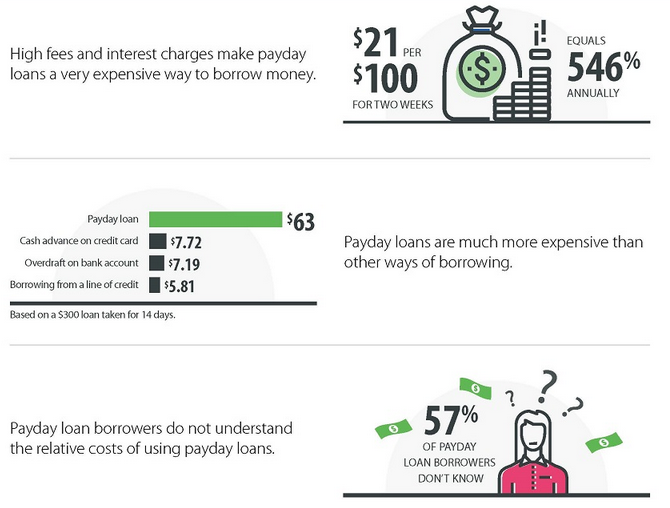

A payday loan is a short-term, high-cost loan. The Financial Consumer Agency of Canada explains that payday loans can let you borrow up to $1,500, with repayment typically due within a short period. The problem is the cost. FCAC’s current example shows that a payday loan can cost around $14 for every $100 borrowed, which is far more expensive than most lines of credit, overdraft protection, or credit card cash advances.

Payday loans are different from regular loans because:

- The repayment term is usually very short.

- You may not need a traditional credit check.

- The cost is often charged as a flat fee instead of regular interest.

- The money is usually repaid from your next paycheque.

- If you cannot repay on time, fees and repeat borrowing can become a serious problem.

That is why I would be especially careful if you are already in a consumer proposal, recently missed payments, or are trying to avoid insolvency. A payday loan may feel like breathing room, but it can also push you deeper into the cycle.

Where Should You Begin Your Loan Search?

If you still have stable income and your debt is manageable, I would usually start with lower-cost options before looking at payday lenders. Banks, credit unions, and reputable loan brokers may offer more affordable borrowing options than payday loans.

That said, traditional lenders may be out of reach if your credit score is damaged, your income is unstable, or you are currently in a consumer proposal. In that case, your focus should shift from “Where can I borrow quickly?” to “What option actually improves my situation?”

For example, someone who only needs a small bridge until payday may compare cash advance apps. Someone who is already drowning in credit card balances should probably look at debt consolidation vs. a consumer proposal or speak with a nonprofit credit counsellor instead.

Best Payday Loan Alternatives in Canada

Here is a quick comparison of common payday loan alternatives. The right option depends on your income, credit score, debt level, and how urgent the cash need is.

| Option | Best For | Watch Out For |

|---|---|---|

| Bank or credit union loan | Borrowers with decent credit and stable income | Approval may be difficult with bad credit |

| Line of credit | Flexible lower-cost borrowing | Easy to overuse if you do not repay it |

| Bree | Small short-term cash advances | Optional express delivery or platform features may cost extra |

| Nyble | Small 0% interest credit-building line | Credit limits are small and optional paid features may apply |

| Credit counselling | People with multiple debts who need a plan | May not reduce principal like a consumer proposal can |

| Licensed Insolvency Trustee | Severe debt, collections, wage garnishment, or insolvency risk | Formal options affect your credit and should be reviewed carefully |

How Can You Improve Your Credit Score?

If you cannot access traditional loans because of a poor credit score, rebuilding your credit should become part of the plan. Canadian credit scoring models are proprietary, but common credit factors include payment history, credit utilization, length of credit history, account mix, and recent inquiries.

In practical terms, the two habits I focus on most are simple: pay on time and keep credit utilization low. For example, if you have a $500 credit card limit, keeping the balance well below the limit is usually healthier than maxing it out every month.

To build momentum, you can use free tools to monitor your progress. Our Borrowell Credit Report Review explains how Borrowell helps Canadians monitor their credit score, flag possible errors, and better understand their credit file.

KOHO may also be worth reviewing if your goal is credit building rather than taking on a payday loan. Just make sure you understand the difference between a prepaid card and a credit-building feature. A prepaid card alone does not work the same way as a normal credit card. Our KOHO Credit Building Review covers this in more detail.

Bree: A Smaller Cash Advance Alternative

For a smaller short-term cash need, Bree may be a cheaper alternative to a payday loan if you qualify and avoid optional fees. Bree currently advertises cash advances with 0% APR and no mandatory fees, with free standard delivery and optional faster delivery.

In plain English, Bree is not a long-term debt solution. It is more of a short-term cash flow tool. That can be useful if you are trying to avoid overdraft fees or a payday loan, but it should not become something you rely on every month.

We cover the details in our Bree Loans Review. The main potential benefits include:

- 0% APR cash advances

- No traditional credit check

- Free standard delivery

- Optional faster delivery

- A potentially cheaper alternative to payday loans for small short-term needs

Nyble: A 0% Interest Credit-Building Option

Nyble is another alternative to consider, especially if your goal is building credit rather than borrowing a large amount. Nyble currently advertises a $30 to $250 credit-building line at 0% interest, with payments reported to Equifax Canada.

That makes Nyble different from a payday lender. It is smaller, more credit-building focused, and not designed for large emergency expenses. Our Nyble Review covers the full breakdown.

Nyble may be useful if you want a small line of credit, credit monitoring, and a way to demonstrate repayment behaviour. But if you already cannot afford your bills, even a small credit line can become another obligation.

Payday Loan Rules Vary by Province

Payday lending is regulated across Canada, but details can vary by province. Whether you live in Ontario, British Columbia, Alberta, Manitoba, Saskatchewan, Quebec, Nova Scotia, New Brunswick, Newfoundland and Labrador, Prince Edward Island, or the territories, check the rules in your province before borrowing.

Some provinces set maximum borrowing costs, cooling-off periods, cancellation rights, or rules around repeat borrowing. The safest move is to check your provincial consumer protection office and compare the payday loan against lower-cost options first. FCAC’s payday loan guide is a useful starting point for understanding the risks.

What Should You Do When Debt Becomes Unmanageable?

If you are using payday loans because your debt has become unmanageable, it may be time to stop looking for another lender and start looking for a debt strategy.

A nonprofit credit counsellor may help you build a budget or set up a debt management plan. A Licensed Insolvency Trustee can explain more formal options like a consumer proposal or bankruptcy. Our Licensed Insolvency Trustee Guide explains what LITs do and when speaking with one may make sense.

You can also read our guide to credit card debt in Canada if your balances are getting out of control.

Need Debt Relief Instead of Another Loan?

If payday loans, credit cards, and cash advances are becoming a cycle, consider speaking with a reputable debt relief organization before borrowing again.

Conclusion

Payday loans may look convenient, but they are often one of the most expensive ways to borrow in Canada. Before using one, I would compare lower-cost options such as a bank loan, credit union loan, line of credit, Bree, Nyble, credit counselling, or formal debt relief.

Bree and Nyble may be useful for small, short-term needs, but they are not magic fixes. If your debt is already hard to manage, the more important step is to understand why you keep needing emergency cash in the first place.

My bottom line: use payday loans only as an absolute last resort, and avoid them completely if borrowing more will only push you deeper into debt.

FAQ About Payday Loan Alternatives in Canada

What is the best payday loan alternative in Canada?

The best alternative depends on your situation. For small short-term cash flow, Bree or Nyble may be worth comparing. For larger debt problems, credit counselling, debt consolidation, a consumer proposal, or speaking with a Licensed Insolvency Trustee may be more appropriate.

Are payday loans expensive in Canada?

Yes. Payday loans are considered high-cost credit. FCAC currently uses an example of $14 per $100 borrowed, which can be much more expensive than a line of credit, overdraft protection, or credit card cash advance.

Is Bree better than a payday loan?

Bree may be a lower-cost alternative than a payday loan if you qualify, use free standard delivery, avoid optional costs, and repay on time. It is still best used for small short-term cash flow needs, not ongoing debt problems.

Is Nyble interest-free?

Nyble currently advertises a $30 to $250 credit-building line at 0% interest. Optional paid features may apply, so review the terms before signing up.

Can I get a payday loan during a consumer proposal?

You may be able to find lenders willing to offer credit, but taking on new payday debt during a consumer proposal can be risky. It is usually better to speak with your Licensed Insolvency Trustee or credit counsellor before borrowing more.

What should I do if I keep needing payday loans?

If you keep needing payday loans, the issue may be deeper than a temporary cash shortage. Review your budget, check your credit report, consider credit counselling, and compare debt relief options before taking on more high-cost credit.

Alex Demolitor is a financial writer hailing from Halifax. Alex has a Bachelors Degree from King's College and passed the CFA Exam Level III. He specializes in fundamental analysis of the stock, bond, commodity, and FX markets. He also covers US & Canadian economic indicators. He has been published on many financial publications, including Investing.com, FXEmpire and others.